As a follow-up to our earlier posting on Customer Driven CRM Mobile App, we propose the architecture elements that enables such CRM app to function. These elements should drive the development of people structure and processes with an effective IT capability as the foundation.

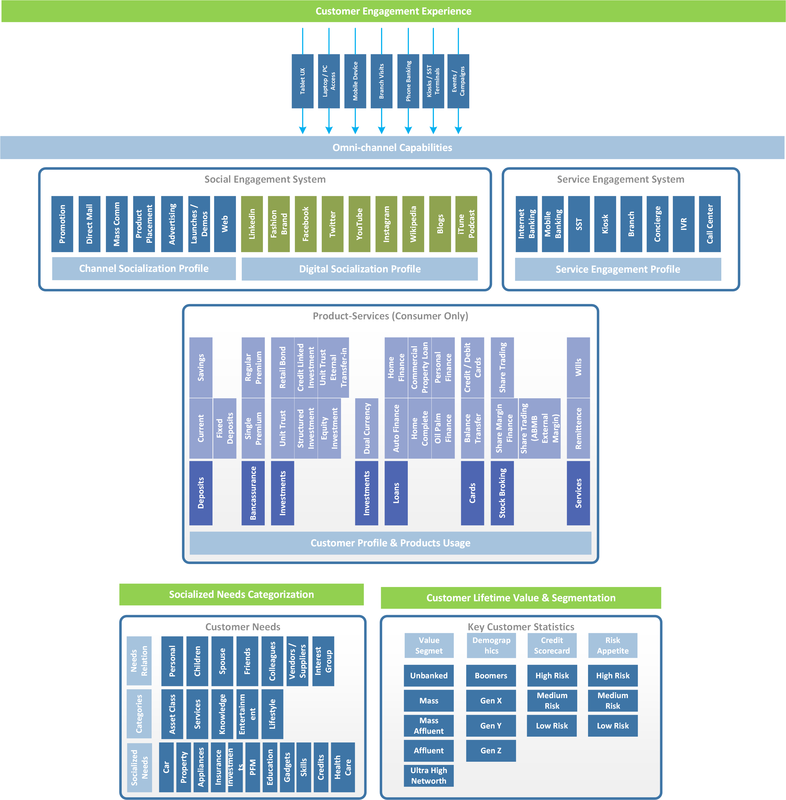

Customer Touchpoints Most organization differentiate between sales engagement and client support engagement. Others have additional functionality around marketing engagement. With mobile and digital technologies, all these functional differences are proving to become a challenge as they continue to function in silo. This is proving costly for banks as all these function are supposed to create a single ‘customer engagement’ capability when combined. For analytic to be effective, all these client facing organization needs to channel their engagement information into a single customer oriented profile. In a nutshell, these profiles are:

Social (Channel & Digital) Engagement Profile Traditional marketing approach advocates non-interactive features such as direct mail, mass media communication, telemarketing, etc. offers little relevance to the individual customer. With such things as spam filters and advertising clutters, customers are increasingly finding the approach annoying (transition phase). The inclusion of social channels as part of banking social engagement strategy is required. Banks have even started to bundle the marketing and socialization messages using banking and e-statements to reduce attrition. By creating a presence and by expanding data analytic into the social space, banks now have an added dimension from which they can evaluate customer value potential and improve share-of-wallet with customer. This could be accomplished through embedding various social channel API’s into purpose built consumer mobile app. At the same time, traditional marketing approach is still used for engaging general mass market customer. Service Engagement Profile It is in the direct customer engagement services where banking relationship is formalized. Customers engagement experience should be assessed and the result of the assessment forms the engagement profile. These are accomplished through a combination of various machine systems (banking portals and self-service terminals) and client engagement workforce (i.e. branch system). The interaction and quality of the interaction has traditionally been measured on a silo perspective. This, in the face, of rising digital importance, is inadequate. The direct channel engagement experience needs to be benchmarked and correlated with data gathered from the other profiles. Client engagement data can provide useful insights in many ways, for example:

Combining Social & Service Engagement Profile When information from both social-digital and channel fabric is combined and used to compute a particular client’s profile, it offers a greater perspective to a client’s lifestyle and service consumption needs. Using techniques such as targeted promotions, socially driven campaigns, purpose built application, etc. a bank is able to construct the needs of the customer. For instance, using Facebook for a marketing campaign, a customer's preference can be mapped when he or she clicks the ‘like’ button on the social message board. This gives the bank a snapshot of the person’s resource motivations. Product Usage Profile Through the use of banking product and services, an individual customer makes available to the bank critical personal information. Although, protected by privacy laws, the underlying bank have the liberty to make use of the data for internal purposes. For this profile, bank needs to capture key information such as the demographics, customer asset and liabilities, collateral, card ownership, car ownership, mortgages, purchasing habits, financial needs, their relationship with other customer, etc. The output of product usage profile needs to translate to customer lifetime value. This quantitative view of the customer enables the bank to evaluate its potential value and its risk to the bank. Such mapping can then be used to target certain customer for further product-mapping and segmentation.

0 Comments

Leave a Reply. |

AuthorDavis Chai is an Architect in the FSI industry for the past 10 years. His career involvement in the industry informed his work and allowed him to contribute to this blog. Archives

August 2017

|

RSS Feed

RSS Feed