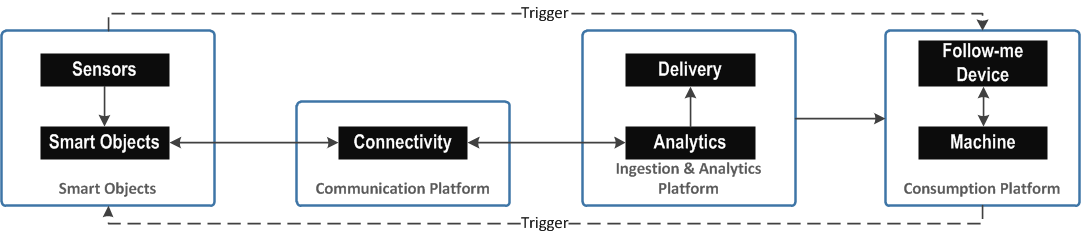

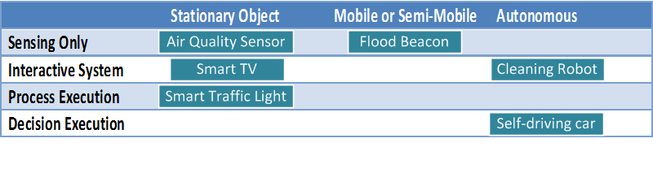

The Building BlocksTo start off, IoT service chain can be separated into 5 key building blocks. The enabling technologies, smart objects, communication platform, ingestion & analytic platform and finally the information consumption and interaction platform.  Smart Objects and ENABLING TECHThe smart objects themselves can be classified into the following type of capabilities (following the works of . Kortuem, G., Kawsar, F., Fitton, D., Sundramoorthy, V.: Smart objects as building blocks for the internet of things. Internet Computing, IEEE 14(1), 44–51 (2010) :

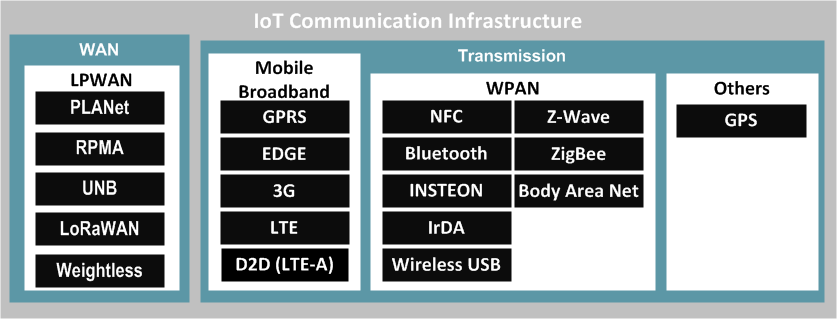

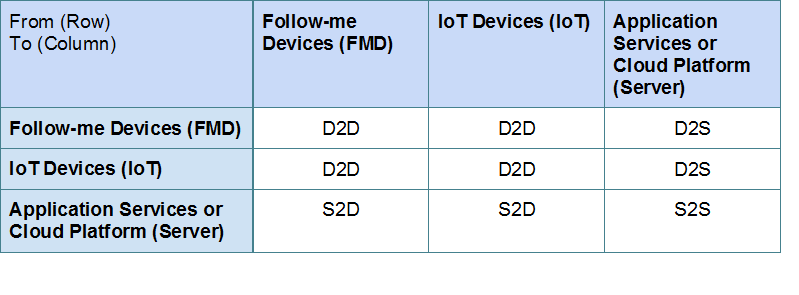

WPAN AND LPWAN for IOTMost IoT deployment currently favors the use of Bluetooth low energy and Wifi for connectivity purpose. Hard wiring will be uncommon except for perhaps stationary use cases. As the LPWAN technology matures, more geographical dispersed IoT devices will also be deployed.  Communications PATHChances are smart objects will not be interacting with human counterparts directly but other non-human entities such as a FMD or application system. This being either unidirectional or bidirectional is as follows:  As shown on the table above, there are 2 main types of D2D, e.g. FMD-IoT, IoT-IoT or FMD-FMD. D2D communication will typically be established by way of WPAN communication technologies such as Bluetooth and Wifi. It is also possible that management of IoT devices be delegated to an application service rather than through an FMD, this is useful for the case where security, automation, multi-device management and higher intelligence are required for IoT action input. This D2S (or S2D) scenario requires application server service - be it on cloud or on private setup or. The choice communication technology and path will have dependency on actual use cases. DECOUPLED VALUE CHAINAs in the case of OTT, the value chain for IoT is separated between the physical and digital information generated. Hence, the 'sensing' only smart objects are really just 'dumb data generators'. The aggregate information presented will be used in combination with other data to provide higher level intelligence and usefulness - making the digital part of the chain more valuable. Most early smart object deployments in the near future will be in very primitive forms - i.e. offering sensing only capabilities. This meant that other platforms are required for the data generated to be processed, useful information produced and finally delivered for consumption by a person or machine. This decoupled value proposition is necessary where the 'dumb' IoT devices itself lacks sophistication to provide intelligence and therefore requires higher plane services such as:

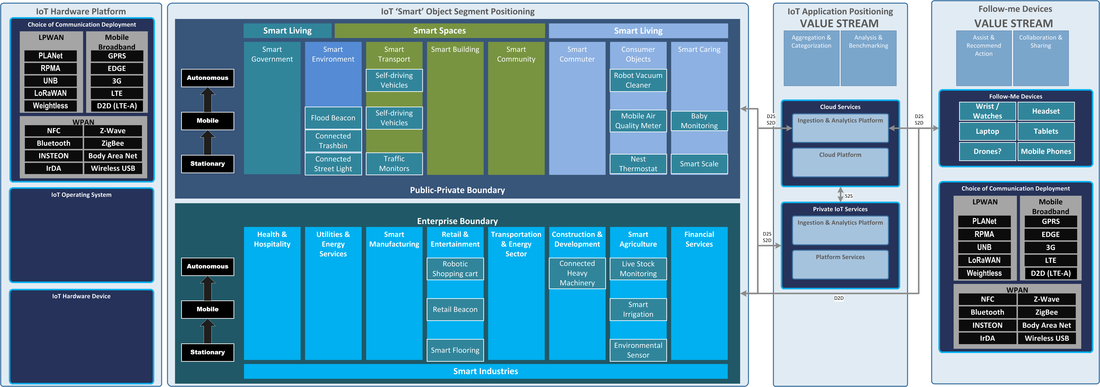

IoT POSITIONING CANVAS Example of currently available Smart object offerings are highlighted in the Smart Objects section.

0 Comments

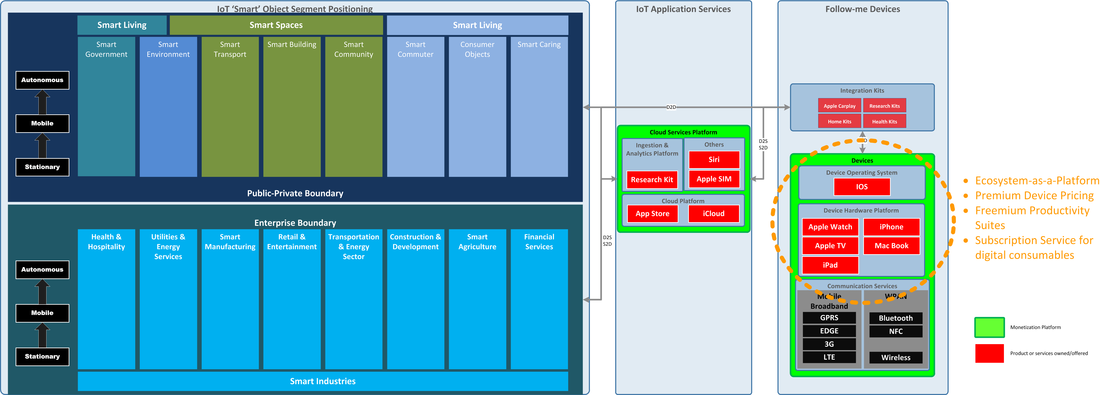

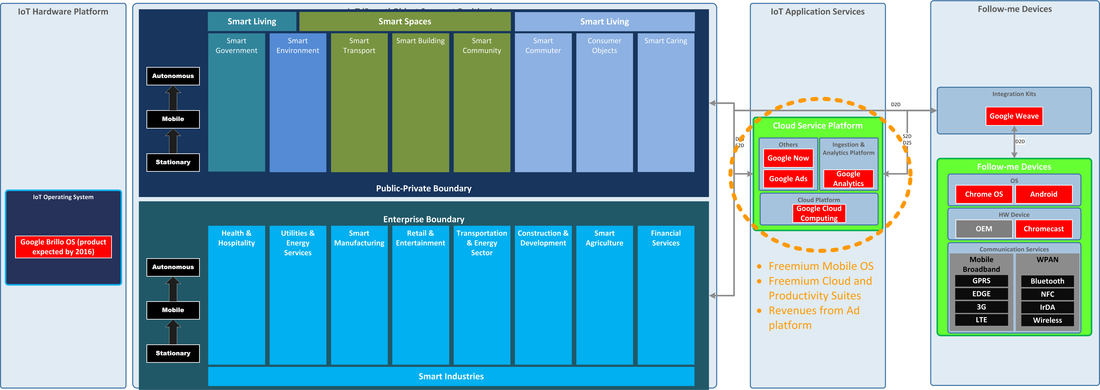

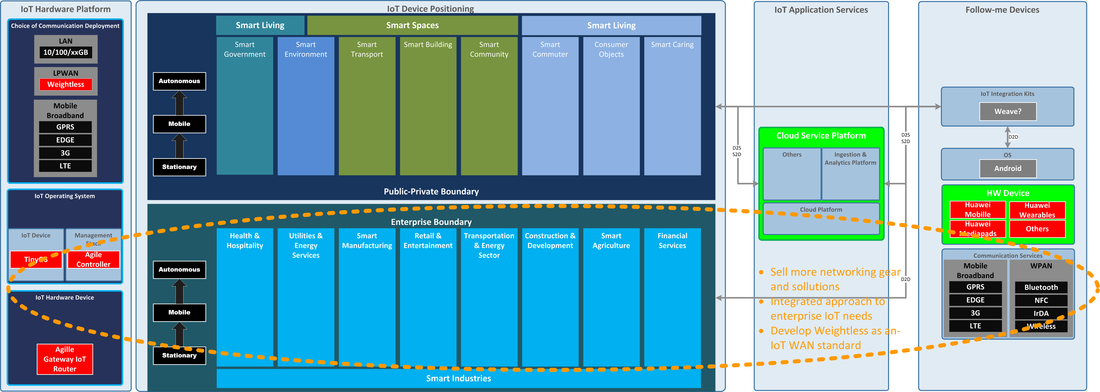

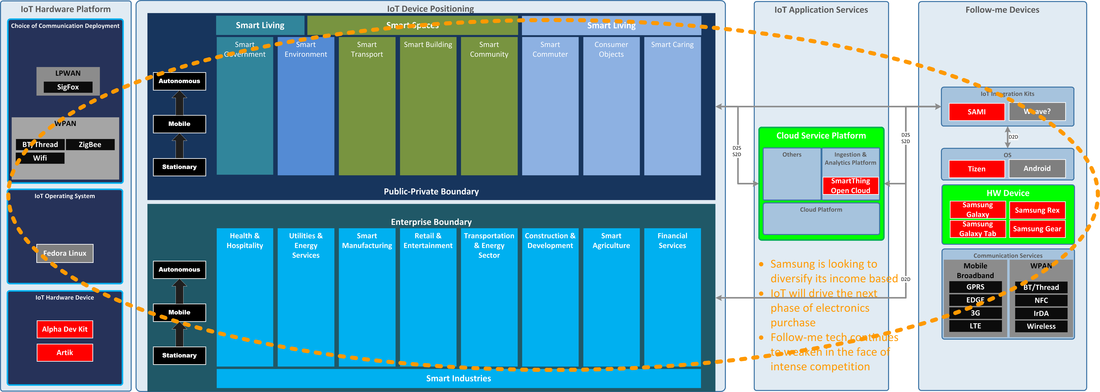

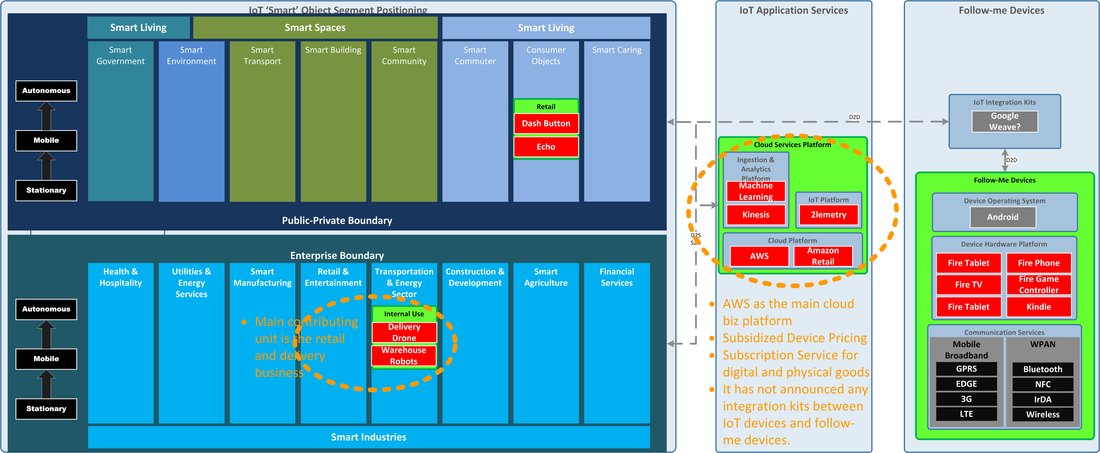

APPLE - IOT TO DRIVE ECOSYSTEM LOCKDOWNThe IoT marketplace is just at its infancy and is set to go through tremendous changes over the next few years. In recognition of that, major tech companies are flocking in with hopes of driving the IoT development direction - much as smartphone technologies have developed over the years. In the following list, I've picked up on 5 IoT heavyweights. Each of these companies approaches and position IoT technologies in their business strategy very differently. First off the list is Apple. Amongst the tech giants, Apple is the only one that offers no direct IoT devices or platform systems. By taking advantage of the strong enterprise endorsement for its follow-me device platform, Apple is extending its arm into Enterprises IoT space via various development kits in an attempt to pull enterprise application developers into its ecosystem. While Apple’s IoT positioning appears defined around its existing profit contributing units, it is also an attempt to ride on the emerging IoT space (keeping a close watch on this market). In the consumer space, Apple’s dominance allows it to easily pull home-based IoT devices and services into its ecosystem. Its HealthKit and ResearchKit is a good example of how an entire ecosystem can bring meaningful changes to the industry. This is carving a strong niche in the Enterprise IoT space.  GOOGLE - IOT AS THE NEXT ANDROID PLATFORMGoogle’s officially entered the IoT scene with its dual announcement of Project Brillo (IoT version of Android) and Project Weave (a new script based language for D2D integration). The choice of Android based platform for IoT smart devices meant that Google will be very much focused on Public-Private IoT space instead of the Enterprise. As with Apple, Google’s current positioning strategy is to drive IoT traffics consumption through its FMD stronghold - Android's. The announcement though lacks clear monetization strategy and how that links to its revenue-earning cloud platform and ad services. The selling point of their current strategy is seamless interoperability through project Weave. Being an open-platform, Google may proof to have the strongest appeal in the public space for smart objects. Yet, there is a lack of Brillo definition around that of LPWAN technologies which is critical for long distance IoT function such as for smart street lights. That said, all eyes are on Google's impact on IoT deployments in Wifi/BT enabled spaces.  Huawei - IOT AS A PRODUCT EXTENSION Huawei provides 3 key solution to the IoT market: an OS platform for IoT devices, an IoT gateway for integrating IoT devices with IP networks and a controller to manage all access to the network including that of IoT. Huawei’s approach is very focused on telco, enterprises and also industrial IoT use cases. Unlike Google and Apple, Huawei’s IoT products are not directed to consumers. The recent acquisition of UK’s Neul shows Huawei’s appetite in maintaining a strong presence in the emerging LPWAN enterprise and telco market. The positioning seems to present a disconnect between its consumer division and its Enterprise division - which, in theory, should offer strong revenue attachment if executed as a combined ecosystem. They are also dependant on 3rd party solution provider such as SAP and Deutsche Telekom for cloud and application integration into their network solution. SAMSUNG - RECREATING THE CROWN JEWELSamsung is hoping to have 90% of its devices connected in the next 2 years. It has recently acquired SmartThing and launched Artik chips to marks its grand entrance into IoT. Being a market leader in the smart phone and consumer electronic space, Samsung seems to have a broad based plan to utilize Artik chips and Smartthing services in most (if not all) its electronic products - including its mobile division. This smart object approach to everything it manufactures is projected to drive 4 key things: new product revenue streams, accelerate electronic product refresh to the ‘smarter’ version, enhance its ecosystem approach to encompass its entire electronic device business and diversify earnings away from its ailing mobile phone division.  Amazon - IOT AS A COMPLEMENT TO ITS BUSINESSAmazon’s choice of IoT market entry stays close to its core business. While it deploys all kinds of product and tools, its core function is always to move more goods and services (with the exception being its AWS offering). This apparently drives its choice of IoT entry as well. Amazon is interesting in that it utilizes IoT deployment to enhance its own retail value chain (e.g. Dash button, Echo, warehouse robotics and more recently, Delivery Drones). Being a full stack cloud service provider, Amazon will also take advantage of AWS in pushing the IoT software agenda. This puts Amazon well ahead of the other players when it comes to cloud IoT strategy. The vertical integration approach by using IoT advancement in retail and AWS for cloud should allow Amazon to accelerate the adoption of IoT-enabled services and in return drive higher revenues.  |

RSS Feed

RSS Feed