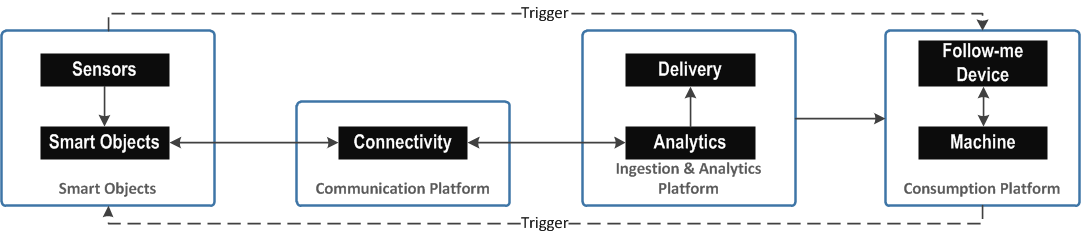

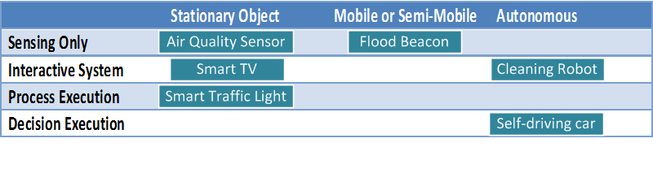

The Building BlocksTo start off, IoT service chain can be separated into 5 key building blocks. The enabling technologies, smart objects, communication platform, ingestion & analytic platform and finally the information consumption and interaction platform.  Smart Objects and ENABLING TECHThe smart objects themselves can be classified into the following type of capabilities (following the works of . Kortuem, G., Kawsar, F., Fitton, D., Sundramoorthy, V.: Smart objects as building blocks for the internet of things. Internet Computing, IEEE 14(1), 44–51 (2010) :

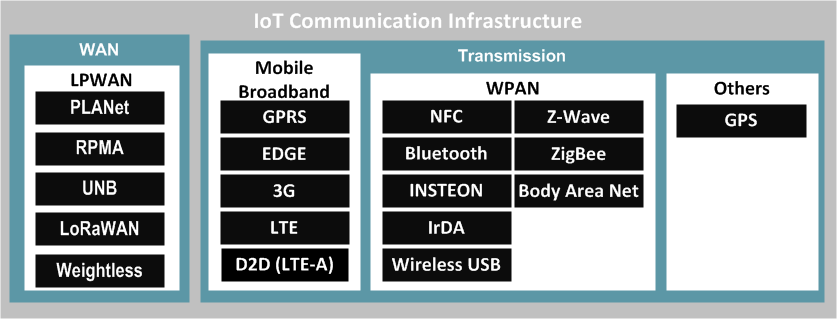

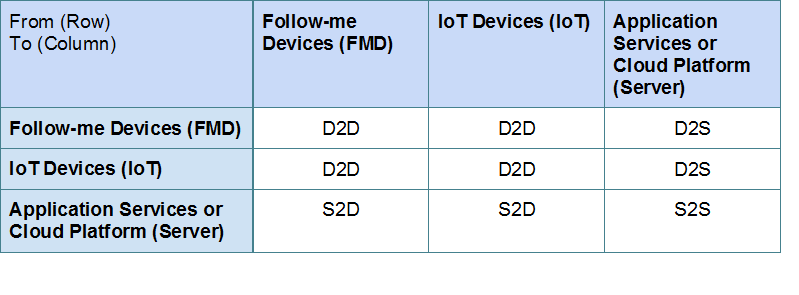

WPAN AND LPWAN for IOTMost IoT deployment currently favors the use of Bluetooth low energy and Wifi for connectivity purpose. Hard wiring will be uncommon except for perhaps stationary use cases. As the LPWAN technology matures, more geographical dispersed IoT devices will also be deployed.  Communications PATHChances are smart objects will not be interacting with human counterparts directly but other non-human entities such as a FMD or application system. This being either unidirectional or bidirectional is as follows:  As shown on the table above, there are 2 main types of D2D, e.g. FMD-IoT, IoT-IoT or FMD-FMD. D2D communication will typically be established by way of WPAN communication technologies such as Bluetooth and Wifi. It is also possible that management of IoT devices be delegated to an application service rather than through an FMD, this is useful for the case where security, automation, multi-device management and higher intelligence are required for IoT action input. This D2S (or S2D) scenario requires application server service - be it on cloud or on private setup or. The choice communication technology and path will have dependency on actual use cases. DECOUPLED VALUE CHAINAs in the case of OTT, the value chain for IoT is separated between the physical and digital information generated. Hence, the 'sensing' only smart objects are really just 'dumb data generators'. The aggregate information presented will be used in combination with other data to provide higher level intelligence and usefulness - making the digital part of the chain more valuable. Most early smart object deployments in the near future will be in very primitive forms - i.e. offering sensing only capabilities. This meant that other platforms are required for the data generated to be processed, useful information produced and finally delivered for consumption by a person or machine. This decoupled value proposition is necessary where the 'dumb' IoT devices itself lacks sophistication to provide intelligence and therefore requires higher plane services such as:

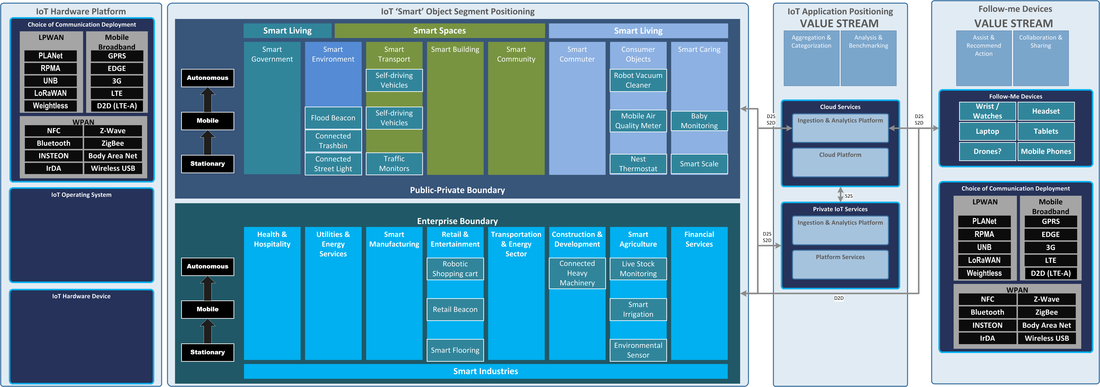

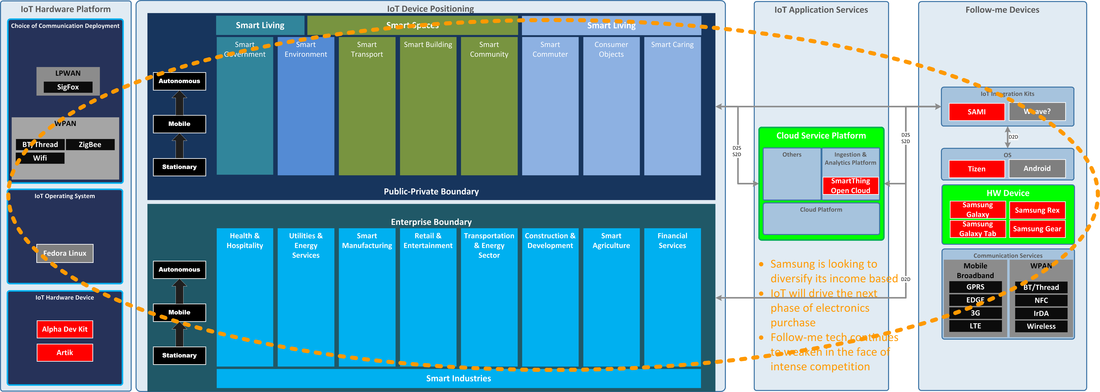

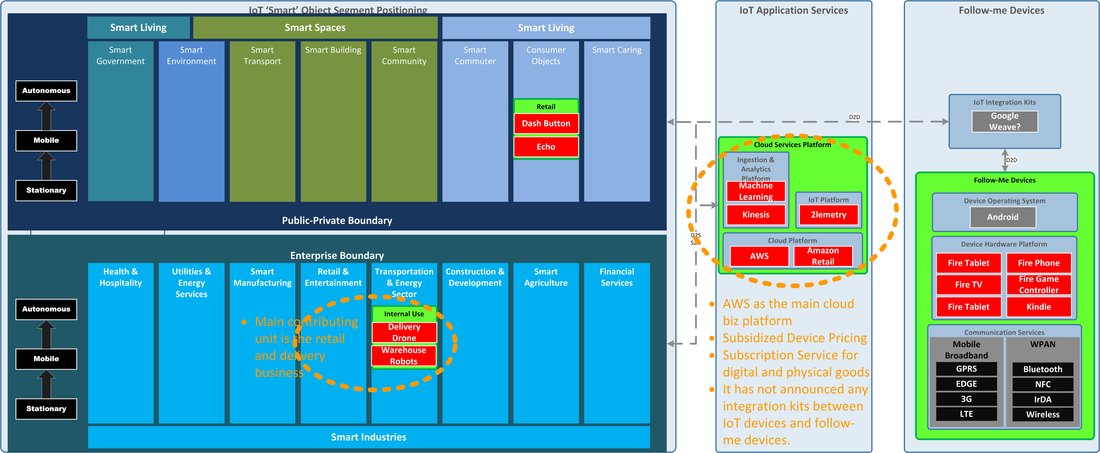

IoT POSITIONING CANVAS Example of currently available Smart object offerings are highlighted in the Smart Objects section.

0 Comments

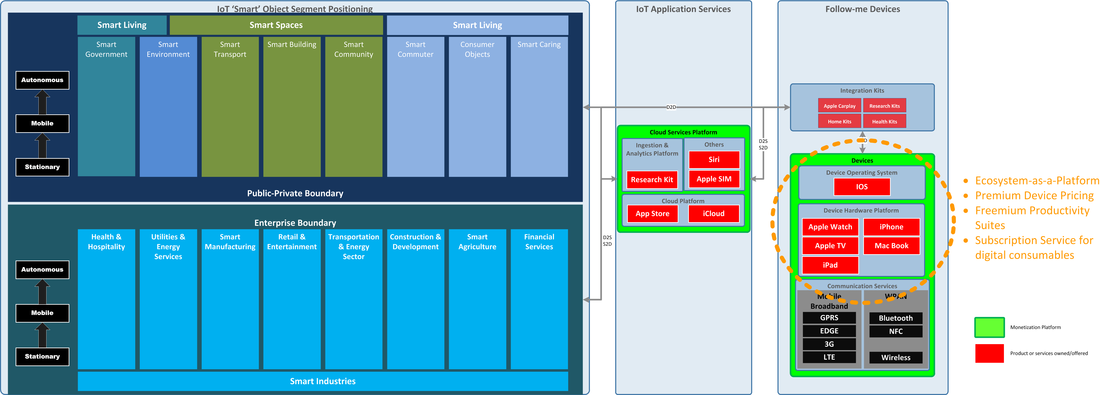

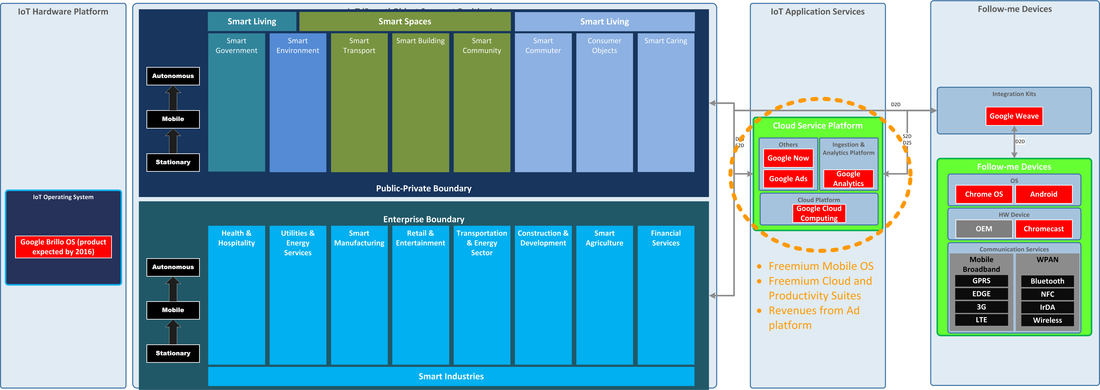

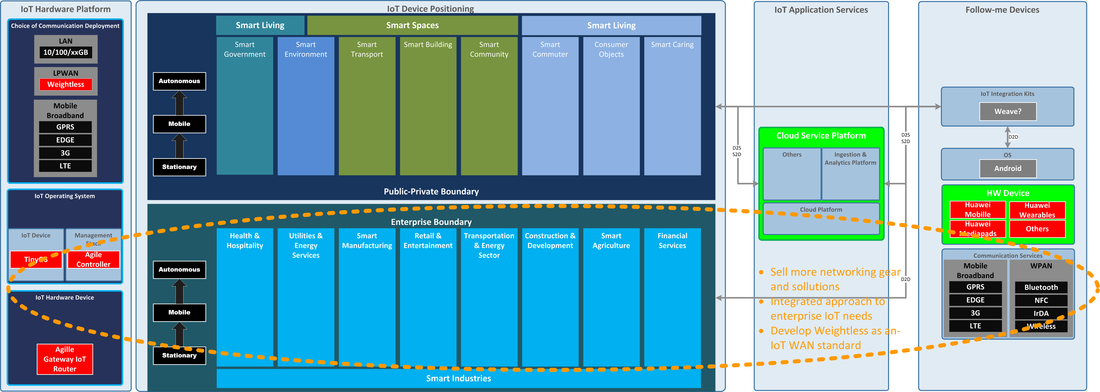

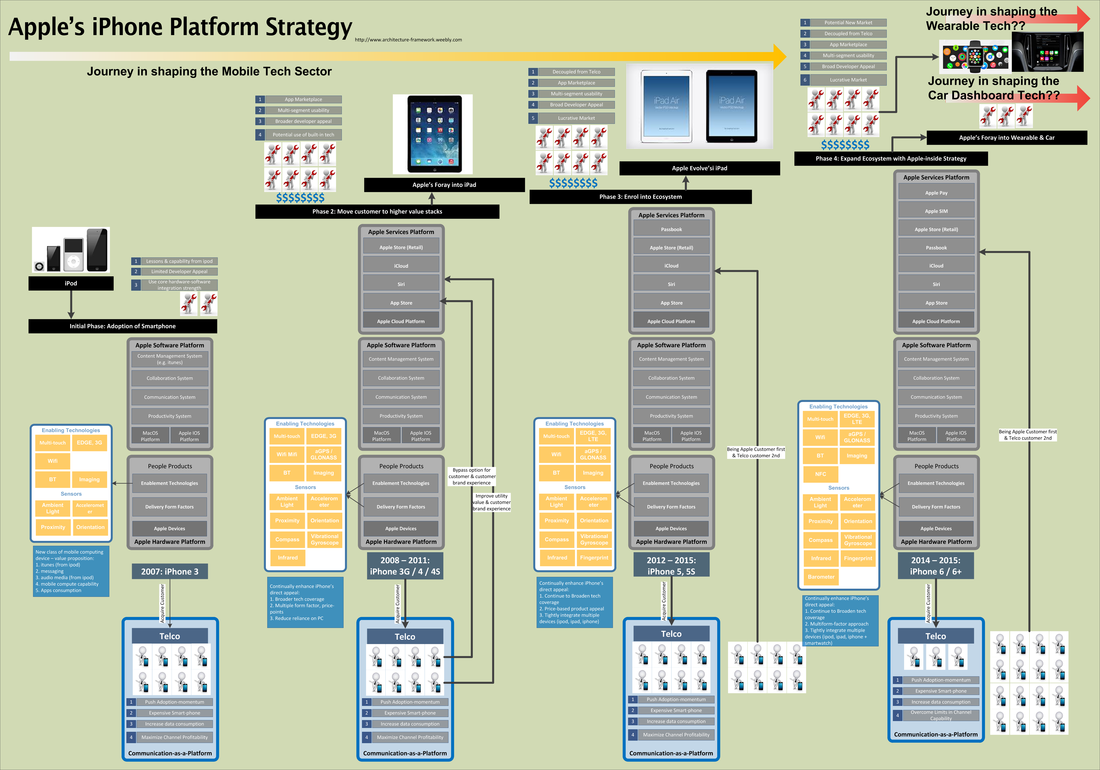

APPLE - IOT TO DRIVE ECOSYSTEM LOCKDOWNThe IoT marketplace is just at its infancy and is set to go through tremendous changes over the next few years. In recognition of that, major tech companies are flocking in with hopes of driving the IoT development direction - much as smartphone technologies have developed over the years. In the following list, I've picked up on 5 IoT heavyweights. Each of these companies approaches and position IoT technologies in their business strategy very differently. First off the list is Apple. Amongst the tech giants, Apple is the only one that offers no direct IoT devices or platform systems. By taking advantage of the strong enterprise endorsement for its follow-me device platform, Apple is extending its arm into Enterprises IoT space via various development kits in an attempt to pull enterprise application developers into its ecosystem. While Apple’s IoT positioning appears defined around its existing profit contributing units, it is also an attempt to ride on the emerging IoT space (keeping a close watch on this market). In the consumer space, Apple’s dominance allows it to easily pull home-based IoT devices and services into its ecosystem. Its HealthKit and ResearchKit is a good example of how an entire ecosystem can bring meaningful changes to the industry. This is carving a strong niche in the Enterprise IoT space.  GOOGLE - IOT AS THE NEXT ANDROID PLATFORMGoogle’s officially entered the IoT scene with its dual announcement of Project Brillo (IoT version of Android) and Project Weave (a new script based language for D2D integration). The choice of Android based platform for IoT smart devices meant that Google will be very much focused on Public-Private IoT space instead of the Enterprise. As with Apple, Google’s current positioning strategy is to drive IoT traffics consumption through its FMD stronghold - Android's. The announcement though lacks clear monetization strategy and how that links to its revenue-earning cloud platform and ad services. The selling point of their current strategy is seamless interoperability through project Weave. Being an open-platform, Google may proof to have the strongest appeal in the public space for smart objects. Yet, there is a lack of Brillo definition around that of LPWAN technologies which is critical for long distance IoT function such as for smart street lights. That said, all eyes are on Google's impact on IoT deployments in Wifi/BT enabled spaces.  Huawei - IOT AS A PRODUCT EXTENSION Huawei provides 3 key solution to the IoT market: an OS platform for IoT devices, an IoT gateway for integrating IoT devices with IP networks and a controller to manage all access to the network including that of IoT. Huawei’s approach is very focused on telco, enterprises and also industrial IoT use cases. Unlike Google and Apple, Huawei’s IoT products are not directed to consumers. The recent acquisition of UK’s Neul shows Huawei’s appetite in maintaining a strong presence in the emerging LPWAN enterprise and telco market. The positioning seems to present a disconnect between its consumer division and its Enterprise division - which, in theory, should offer strong revenue attachment if executed as a combined ecosystem. They are also dependant on 3rd party solution provider such as SAP and Deutsche Telekom for cloud and application integration into their network solution. SAMSUNG - RECREATING THE CROWN JEWELSamsung is hoping to have 90% of its devices connected in the next 2 years. It has recently acquired SmartThing and launched Artik chips to marks its grand entrance into IoT. Being a market leader in the smart phone and consumer electronic space, Samsung seems to have a broad based plan to utilize Artik chips and Smartthing services in most (if not all) its electronic products - including its mobile division. This smart object approach to everything it manufactures is projected to drive 4 key things: new product revenue streams, accelerate electronic product refresh to the ‘smarter’ version, enhance its ecosystem approach to encompass its entire electronic device business and diversify earnings away from its ailing mobile phone division.  Amazon - IOT AS A COMPLEMENT TO ITS BUSINESSAmazon’s choice of IoT market entry stays close to its core business. While it deploys all kinds of product and tools, its core function is always to move more goods and services (with the exception being its AWS offering). This apparently drives its choice of IoT entry as well. Amazon is interesting in that it utilizes IoT deployment to enhance its own retail value chain (e.g. Dash button, Echo, warehouse robotics and more recently, Delivery Drones). Being a full stack cloud service provider, Amazon will also take advantage of AWS in pushing the IoT software agenda. This puts Amazon well ahead of the other players when it comes to cloud IoT strategy. The vertical integration approach by using IoT advancement in retail and AWS for cloud should allow Amazon to accelerate the adoption of IoT-enabled services and in return drive higher revenues.  By the launch of iPhone, Apple's iPod and iTunes is already a dominant force in the portable media players market - which literally redefined the digital entertainment industry. Apple made good use of these capabilities in the launch of iPhone project. Their undisputed edge in combining art with science meant that they can create many more sexy products. However, good looking product can only do so much but great products carries with it great utility value. Likewise iPod was a great product because of its revolutionary user interface and Apple's leadership in driving a whole new way in which digital medias are bought and consumed. Apple took these lessons and used it to create some of the most exciting product in the history of mobile communication - the iPhone. The iPhone business strategy and architecture is probably very widely analyzed and documented. What the following article will do is provide an insight into how Apple will continue to engage its customers and build stronger product/profit pipeline, well beyond the iPhone success story.  Strategy & Architecture That Built the iPhone Empire Apple probably have a bunch of interesting technologies available to it long before the launch of iPhone. Instead of just focusing on selling a feature packed smartphone, Apple had their eyes fixed on the bigger pie and took great pains to re-architect the market structure it sees as posing bigger challenge to its market ambition. The effort in reengineering the both the iPhone and its marketplace took place over more than 10 years time-span and can be broken into multiple phases. Phase 0: Creation & Positioning The technology that created the iPhone itself meant that Apple had to look at the product market very differently. Multitouch screens and compute capacity meant that this is less of a phone than a mobile computer. iPhone is also positioned as the smartphone with highly recognized entertainment feature by featuring iPod technologies. At the same time, Apple picked up a bunch of enabling tech aimed at making iPhone an electronic 'Swiss-army' knife - accelerometer, light sensors, camera, Bluetooth, proximity sensors and orientation sensors. Initially, iPhone presents simpler apps and specification, one that is nudging slightly towards being 'cutting-edge'. This is understandable given that this concept is relatively new to the market and lacks 3rd party developer community support. It also meant that Apple had to develop and market productivity suites by using a combination of existing Apple productivity suites and developing it from scratch - visual voicemail, threaded text messaging and safari browser. Phase 1: Market & Accelerate adoption Apple probably saw that the key challenge was that telecommunication industry was a very vertically integrated sector. Since its a mobile computer, iPhone needed developers to push up its utility value by creating apps. The iPhone was meant to decouple the vertical integration from day one. But Apple needed an accelerated adoption cycle and customers and VAS developers back then are largely locked behind the Telco. Taking into account the fact that the iPhone will consume a lot of mobile data (based on standards back then) and being pricier than the standard feature phone, the Telco-Apple alliance seemed inevitable. Phase 2: Build presence and Platform The accelerated adoption by the time they launched iPhone 3G showed that there is a strong appetite for mobile data and apps consumption - for convenience, productivity and entertainment reasons. In this phase, Apple took advantage of the trend and started to move customers to higher level service stacks by launching the App Store and later iCloud and Siri. These cloud services enabled customer to extend the value of the smartphone beyond its physical limitations. The iPhone by now is packed with additional electronic components such as GPS, Gyroscope and Infrared sensors that allowed developers to create new functionality and apps. Drawn in by the monetization scheme, these developers created a number of interesting and useful iPhone application and in return drew in larger and larger number of users. This approach created a self-reinforcing customer-feature-functionality build-up cycle. Telco at this point is still happy to indulge in the business created by Apple iPhone's - even when the Telco VAS value chain is completely broken and its traditional communication business slowly being chipped away by OTT players through the App Store and Google's Android platform. Phase 3: Gear-up for Ecosystem Integration At this stage, customers are already familiar with the App Store and the some of the early forms of Apple cloud services such as Siri and iCloud. Apple introduced Passport to the cloud family. The productivity suite offered by Apple is now being bundled away for free. Apple is also learning that there is only so much of technology marvel they can pack into a device in a short time window - there is a diminishing return in this approach. Nonetheless, fingerprint sensor and LTE support was added. Tech enthusiast was not very impressed. Phase 4: Prepare for the Next Big Launch Apple sidestepped a bit at this stage by creating different form factor in a move to counter the slowing sales and waning interest. This cannibalized certain Apple product such as iPad but gave it sufficient breathing space until the next launch. The fingerprint sensor now has a companion app called Apple Pay. This combo although revolutionary, was still incomplete. Apple have also added Barometer into its arsenal of sensor wizardry. This, however, has less to do with assisting mountain climber but a preparation for what comes next - in the name of science, fitness & healthcare. Other services launched include Apple SIM which other than is an attempt to simplify its device design, is probably also related decoupling product design from to the next product launch. Not only did Apple manage to create a great blockbuster product but in every step of the way they have created utility values to their customer. This approach allowed customer to continuously reap benefit and value out of owning an Apple product while generating steady revenue streams through App Store and iTunes. Post-iPhone 6 & 6 Plus The battle in telecommunication device space is largely won and along with it the communication industry transformed to the standard defined by Apple. At the same time, the mobile computing industry is disrupted and transformed in the face of Apple's iPad. And certain industry vertical such as retail and education is still feeling the combined impact of iPhone and iPad's. Being the size that Apple is today, the next move will not be any less disruptive and will probably bigger and bolder. In the next section, we will attempt to use some architectural basis to determine what and how Apple's next move is going to look like. It will, hopefully, allow us to make sense of the potential magnitude of Apple's entry into wearable market itself.  Strategy & Architecture That will go Beyond Building the Apple Watch Empire

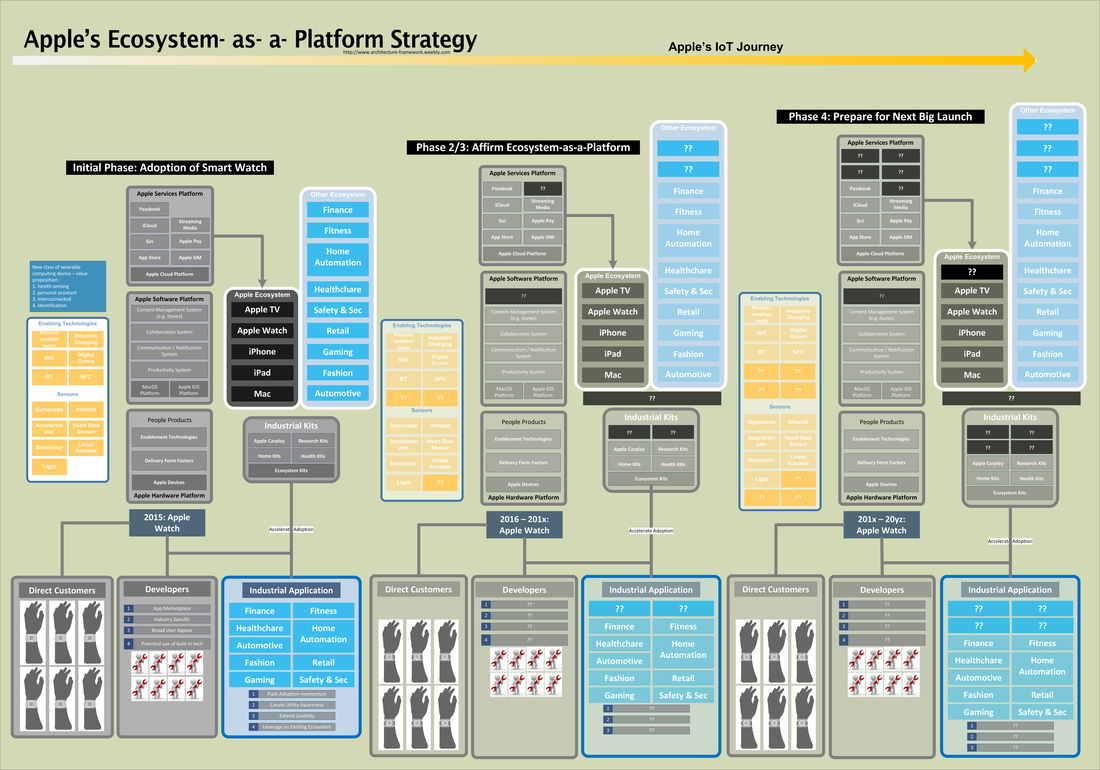

At the onset of the Apple Watch launch, Apple is already a dominant force in Smartphones and Mobile computing through iPad and Mac. They have geared up product integration by moving services up the cloud and offered most of their key productivity suites as giveaways. The mobile telecommunication standard is continually being challenged by smartphones and in particular the high standard that iPhone has set while. Apple at this point is not contend to settle with just the iPhone success and is already on its way engage a very different market segment - the wearable market. Step 0: Positioning Similar to baby years of iPhone, Apple Watch needed accelerated adoption. To achieve that, the barriers of adoption must be lowered - cost, usability, interoperability, learning curve, etc. Unlike other vendors, Apple had their eyes fixed on creating pipeline not one-time blockbusters. This time, however, the strategy will not be about moving customer to the highest service stack (as in the case of iPhone) but towards a more sophisticated and highly evolved strategy - the ecosystem strategy. Apple's initial foray into the SmartWatch market can be broken into two groups of target customers:

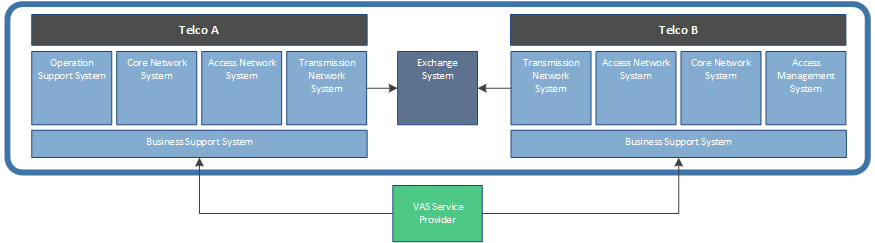

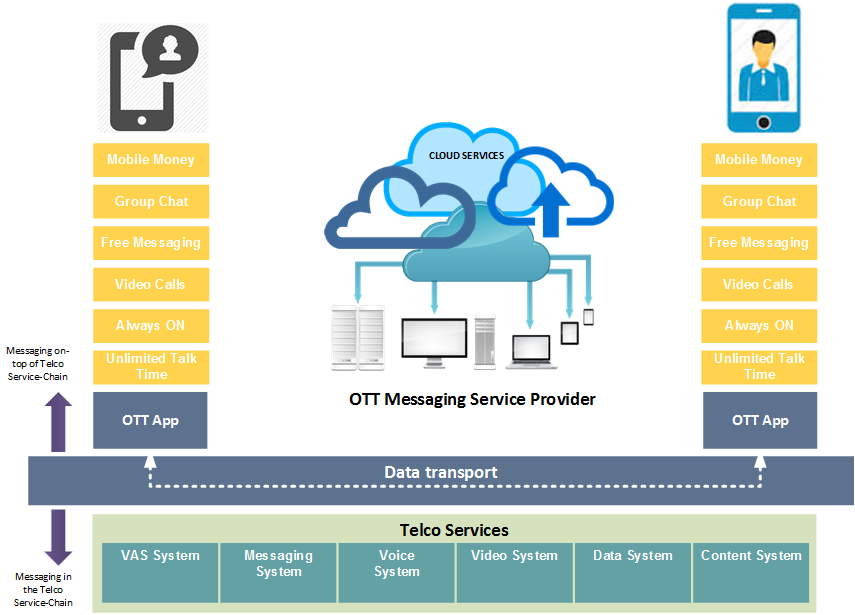

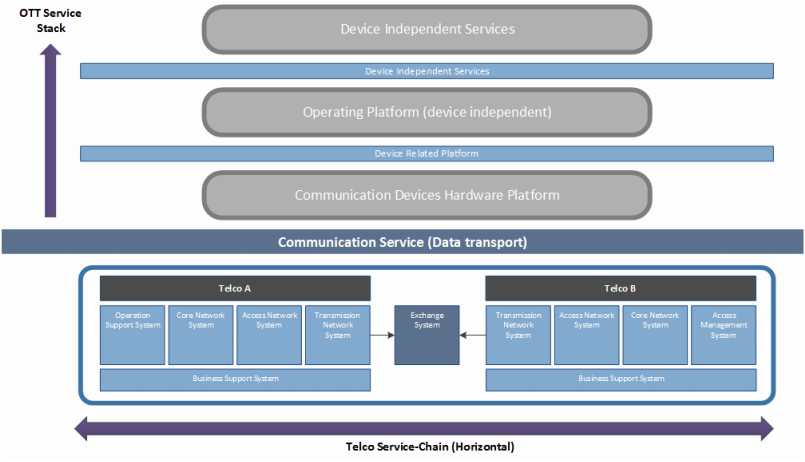

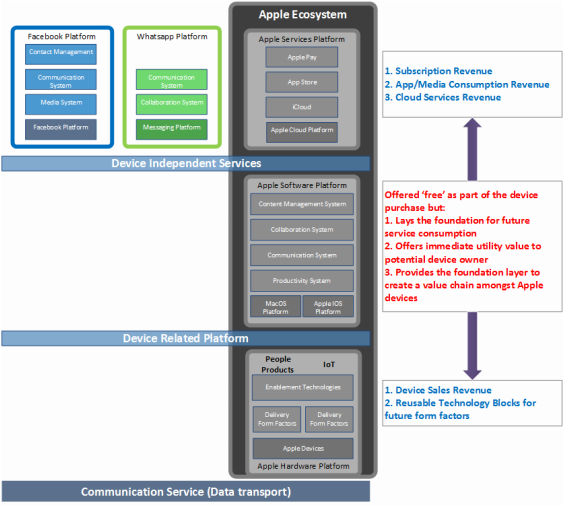

Phase 1: Provoke & Accelerate adoption The continued build up of Industrial-level cooperatives and partnership showed that a high degree of market re-engineering is required for this device to be highly successful. This is precisely what Apple does best and is already doing over the past months leading to the official launch of Apple Watch. The Apple move is also seen as extending out of the directly linked markets - such as with its ResearchKit, CarPlay, AppleTV and HomeKit. Phase 2: Build presence and Ecosystem For a start, the watch itself will be of limited capability and requires integration with other devices to create new meaning and deliver new insights. Apple would continuously enhance the Apple device ecosystem integration as an ongoing effort to draw in more industrial relevance. While device enhancement through sensors and other technology pieces provides the key enabling technology, software that allows the devices to interact with one another is key too. This improvement is performed in parallel to design decisions to counter movements by other Smart Watch players. Nonetheless, all these could just be a smokescreen of what Apple is actually building. By this phase, Apple would have slowly but surely be moving customer to a new platform that is not even a single product to begin with - but a platform of a diverse digital ecosystem. Phase 3: The Ecosystem Battlefield The industry partners may or may not be aware that at this point, Apple would have locked itself in the value chain of a few key industry verticals. Their customers are now part of Apple's ecosystem platform subscriber. These industry never have the means to connect with their customer and have never been so dependent on a consumer product manufacturer in its value chain. Probably more than a few industry would have been disrupted by now. Competitors and industry incumbent will be scrambling to develop their own Ecosystem platform to counter or take advantage of the disruptive wave. The Apple Watch would continue to evolve and gain new level of device sophistication through addition of hardware and software capabilities. The combination of hardware, software, developer and industry participation meant that the Ecosystem is continuously being enriched and evolves. Phase 4: Prepare for the Next Big Launch If Apple successfully executes on its vision and the Ecosystem became a reality, we would be witness to probably the first consumer-product driven IoT. Not only would Apple products become ubiquitous but the level of industry integration will be unparalleled. Yet, I bet you that Apple would have its eyes on the next big launch and is already laying the foundation for that.  Horizontal Service Chain In the early days, when mobile devices are not 'smart' and internet accessibility was limited, these devices and their respective VAS providers provide the critical 'service-chain' in order for customer to receive full telecommunication service experience (e.g. content delivery, voice mails, call chargeback, etc.). These VAS services and sales of handsets creates additional revenue to telcos. Partnership with mobile device manufacturer have not only allowed telco's to earn additional revenue out of handset sales but also created a steady revenue stream by packaging voice, data and messaging services into contracts. In return, handset manufacturer gain access to local markets without needing to build expensive retail presence and cut short the sales and adoption cycle. Technology Forces Breaks Service Chain As smart phone technology and internet services evolved, this service-chain by telco is gradually broken. The emergence of IP-based data access as the dominant form of service consumption enabled OTT players to dominate. This is possible as services can now exist in a higher plane than that of the transmission and access network - decoupling of the service layers in good old OSI-fashion.  To VAS or not to VAS Although OTT have long existed and was mostly confined to desktop/laptop computing, the threat to telcos came to light when mobile handsets themselves wield the technology and communication capability required for OTT players to offer disruptive telco services. The OTT players are now dominant in voice, video, messaging and other familiar telco revenue territories. The telco-VAS alliance is weakened as OTT continues to erode their operating margin. With fundings and revenue opportunities, the OTT industry continue to attract new players. Now, you can almost find an OTT service provider for each class of services offered by a traditional telco (a short list is as shown in the diagram below). The challenge was not so much the entry of the OTT themselves but the value driven business model that they are pursuing by taking advantage of the internet.  OTT Service Stack OTT services are not a single stack of services. It is a combined complementary stack of technology advancement. The OTT service stack consists of: 1. Communication Devices HW Platform - the one directly above communication service stack 2. Operating Platform - the one above HW device stack 3. Device Independent services - the one above the Operating platform stack  In order to drive more traffic to OTT services, they have to focus on attracting large user base by value adding heavily. Their revenue model is also mostly asymmetrical in nature in that they cross subsidize one product in order to attract subscription or revenue in another. Some times, the OTT service providers rely only on advertising revenue. Telco needs to understand the impact of OTT service stacks. As-a-Platform or As-an-Ecosystem Today, the OTT themselves have evolved and have mostly settled in either a platform (OTTP) or ecosystem (OTTE) format. Some have a combination of both (OTTEP). Apple as OTTEP Take for example, Apple's combined ecosystem and platform approach. The apple ecosystem is an engine that drives revenue from both the Apple Services platform and Apple Hardware platform stack but offers Apple Software stack for zero direct fees. In other words, Apple is giving away its software platform in order to drive sales at the top and bottom stack of its ecosystem. Some of these software services are in direct competition with Telco services - e.g. Facetime. As a device manufacture, Apple also allow other device independent services to operate atop its software platform e.g. Facebook and Whatsapp. More to the appeal of Telco is the revenue opportunity by "subscribing" into the Apple ecosystem model - hardware sales & data subscription/consumption. Less important is the extent of Value Stacking and Platform establishment by Apple and the amount of control that Telco will cede to Apple's ecosystem. The irony here is, each devices that the telco sells potentially erodes the revenue from telco services.  Telco willl continue to focus on its core capabilities that is providing connectivity and access. While their focus is still fixated on current blockbuster product/services, their value proposition will be limited as they choose to operate within their service-chain boundary. The digital world requires telco to rethink their role within the industry and along the service stacks. There is already evidence of their eroding role as the cost of delivering data services is not equaled by what they have earned from selling data.

|

RSS Feed

RSS Feed