|

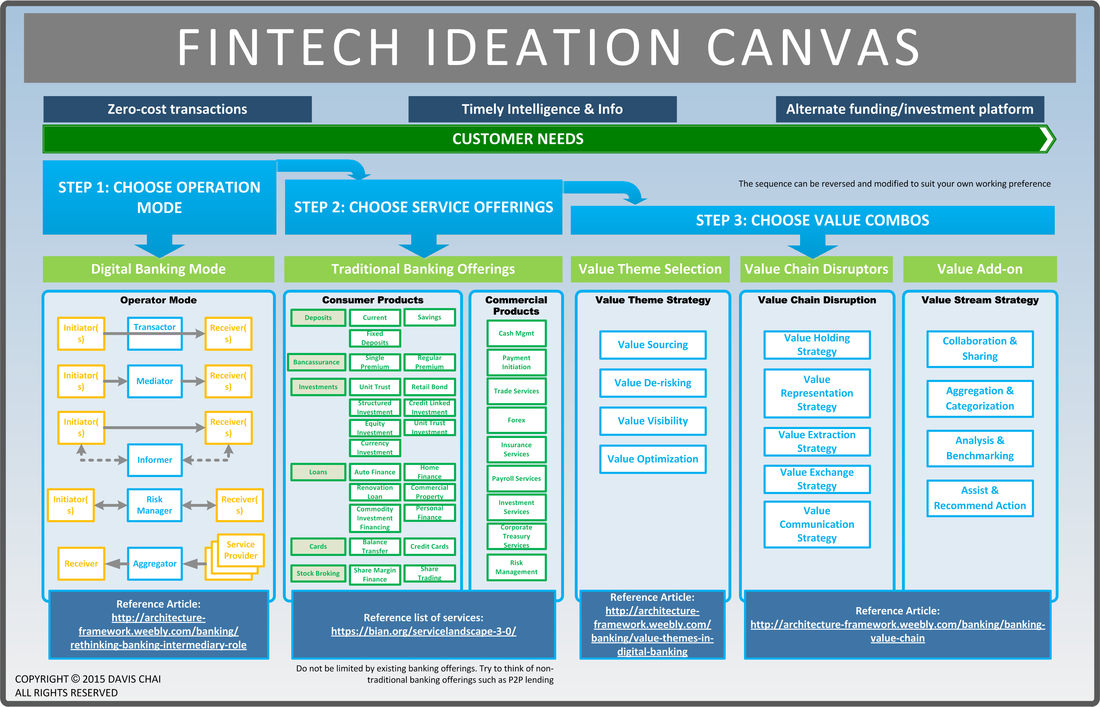

To all budding Fintech entrepreneurs and enthusiasts, here is a fintech service ideation canvas for you to kick start that million dollar business!

0 Comments

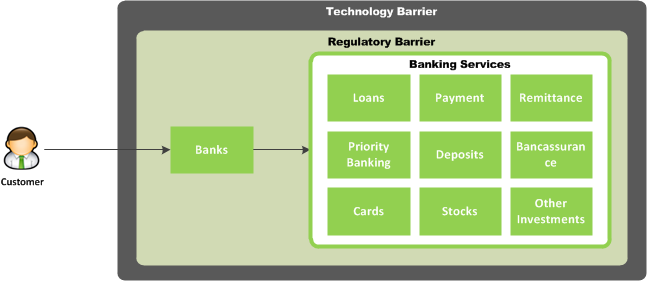

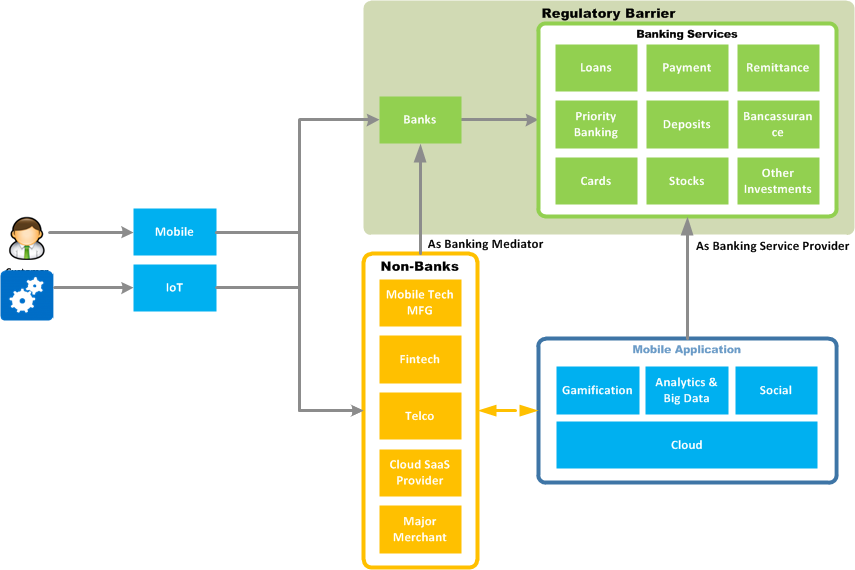

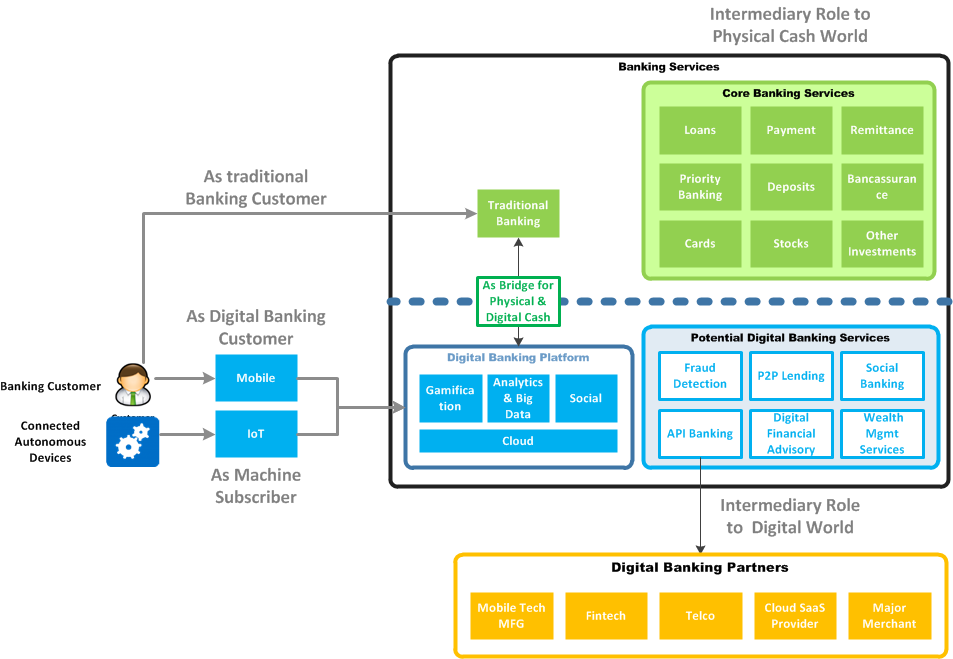

Up until the early stages of internet boom, bank still enjoyed near monopoly of access channel to all banking related services. Most banking customers rely on such channel services as banking kiosks/branches, cards/POS terminals, ATM, banking e-portal, etc. to gain access to financial services. Technology advancement have since made it possible for customers to receive banking services in their own convenience. Whilst the bulk of the mobile technology advancement occurred in the consumer space, adoption by banks is largely fashioned around traditional business lines. Thus limiting its full potential. As banking customer increasingly embrace digital lifestyle, banks appeared to have lagged further behind. Non-banks sees this as open opportunity to offer banking related services in ways that is not offered by banks.  Banking Technology Barrier is in a peculiar way, lowered for non-banks but raised for banks (mostly due to the lack of an effective approach to digital banking). The world of banking is thus opened up to non-banking competition. These opportunistic players were quick to adopt technological advances made available to both consumer and to themselves as service provider. These non-bank players either enters as intermediary to banks (e.g. Apple Pay, Square, Billguard, Google Wallet) or provide certain forms of services in direct competition to banks (e.g. LendingClub, Bitcoin, Venmo). Cloud services are being consumed by both enterprises and end-users as a way to leapfrog technology adoptions (changing from tech purchasing to tech consumption). To further capitalize on the technology gaps opportunity, non-banks uses Value Stream approach - which encompasses the ability to: 1. Collect, aggregate and categorize information 2. Analyze, benchmark and offer intelligent insight into information 3. Offer collaborative and sharing functionalit 4. Drive behavior by assisting and recommending actions Rather than become sidelined by non-bank digital players and missing out on revenue opportunity, banks should develop a more holistic digital banking strategy. This strategy does not necessarily need to alienate traditional banking services but complements or takes advantage of it. Banks should take this opportunity to consider its strategic banking touch points and focus on the emerging banking role as financial intermediary in the digital world. More importantly, banks should use this positioning as a way to learn and evolve its value creation capabilities.  Banks can bridge the digital gap with the physical cash world. There is already a growing trend of ATM machines being used to interact with digital world - e.g. SMS cash withdrawal, use mobile phone for authenticating. For housing loan and consumer credit, banks can consider alternative funding source - e.g. collaborative funding or P2P in short. They could use technology to assist in onboarding new customer, client repayment handling, personal finance management purposes, etc. They could also make good use of core capabilities such as in fraud detection and risk management. These too can either be exposed via banking API for merchant/partners to subscribe and use or be embedded as part of transactional banking function much as what BillGuard has done. Banks should embed transactional banking function as part of an-Open API service for non-banks to use. By doing so, banks would be plugging themselves in to a larger digital ecosystem. To the end-user, services such as PFM and private wealth management from partner companies will become more useful when they have access to banking data.

|

AuthorDavis Chai is an Architect in the FSI industry for the past 10 years. His career involvement in the industry informed his work and allowed him to contribute to this blog. Archives

September 2017

|

RSS Feed

RSS Feed