The Mass Market SegmentThe millennials (born between 1982 and 2000) who are mostly at prime working age now, are often the focus due to the segments importance in sustaining the chain of disruptions. According to Teaching Financing Tools concept (source: https://www.joe.org/joe/2013february/tt6.php) this group who have a tendency to overuse credits, lacks emergency savings/funding, lacks insurance protection, focused on current needs instead of the longer term needs, etc. Hyperbolic discount tendency is largely at play here. Being economically less viable and out of reach by mainstream financier, alternate financing method such as usage-based services, peer-to-peer and crowd-sourced becomes more appealing. Take-up rates of these services indicates this group’s willingness to go for higher-risk options in order to satisfy consumption needs. Arrival of fintech platforms coincides well with many (if not all) of them. With a strong appetite for debt driven instant gratification, many will be left with little cash for shocks in later life. Such group represents risky but attractive high-interest paying market segments for emerging platform players. The Traditional HNW or UHNW SegmentOver the years, many established investors have grown wary of financial advices delivered by FSI. Clients are no longer satisfied with receiving monthly statements of paltry investment return in their mailbox. Investors want to be able to use their data to look at outcomes in real time. Customers can now quite easily obtain reports and insights that would have previously been hidden or expensive to obtain. Technology is the primary enabler – the use social media, search, and mobile apps during an investment journey, and the proliferation of seamless, omni-channel digital experience lets them interact with service providers anytime, anywhere, and on their own terms. Customer can now shop and compare in the open marketplace to determine which product or service offers the best value for money. This group may stay on course but are increasingly more adept at engaging fintechs, P2P, crowdsourcer, etc. as net financier. Robo-advisors are now gaining grounds and providing really low-cost fees in financial investment areas that require little or no advisory services. The Emerging HNW SegmentWith the old economy disrupted and new class of wealth created, we will be seeing an emerging group of young U/HNW entrepreneurs who is armed with plenty of liquidity and know-how. Having carved out their own existence and survival in a highly volatile and hyper-competitive world, this group of generally young individuals will drive unique wealth management needs – it will be highly international, dynamic and complex in nature. They are probably the least tolerant of time-consuming and complicated processes; have very low trust and are especially vulnerable to exploitative motivation shown by traditional wealth managers, e.g. selective information disclosure and not given proper advise/control of financial decisions. To make it even more challenging, the kind of value they place on life is more subjective than that of the earlier generation. Enablement DrivenAs the ability of robo-advisors and robo-managed investments improves further in the coming years, the need for human intervention will be reduced. Although the promise of ultrahigh returns will be diminished as these programs are algorithmically built to balance risk with returns, it remains attractive as it promises long term growth. This frees up critical human capital to consider and tackle the issue of complex investment needs.

As better endowed generation grows to favor quality of life over wealth and capital accumulation, they will increasingly consider putting their money on social causes, believes and create meaningful impact. Although personal and family financial need is still the main priority, this emerging group takes a mixed world view: one that is driven by the hardship seen in the past decades and one that considers money as just a means to an end. With the passion and intent to drive ‘meaningful change’ this group of like-minded people presents an emerging opportunity. There are already various avenues in the market that caters for their needs. RBC that provides investment products to investors around the world released a survey report in November 2016 entitled Near-Term Uncertainty, Long-Term Opportunity. The report indicates that investors want more information showing how they can use their capital to achieve positive change while growing their assets. To start with there is the impact investment or socially responsible investment platforms. Such investment platforms are spearheaded by either market-benchmarked performers or non-profit believe groups. This would have appealed to HNW individuals and HNW family institutions. Then there is the smaller retail investment groups, the mass affluent who will collectively make smaller impacts. Through such platforms as kickstarters, peer-to-peer and online investment platforms, they too are able to drive impact without sacrificing returns. The shift is small, but the trend may be lasting and will continue to grow. The emerging HNW and UHNW groups will set the investment tones for coming years, one that is bound to focus on the qualitative factors surrounding socially sustainable and regenerative wealth. Equipped with A.I., robotics and wealth management expertise, the generation seeks not just returns but a platform that 'enables' them to realize their own world vision.

0 Comments

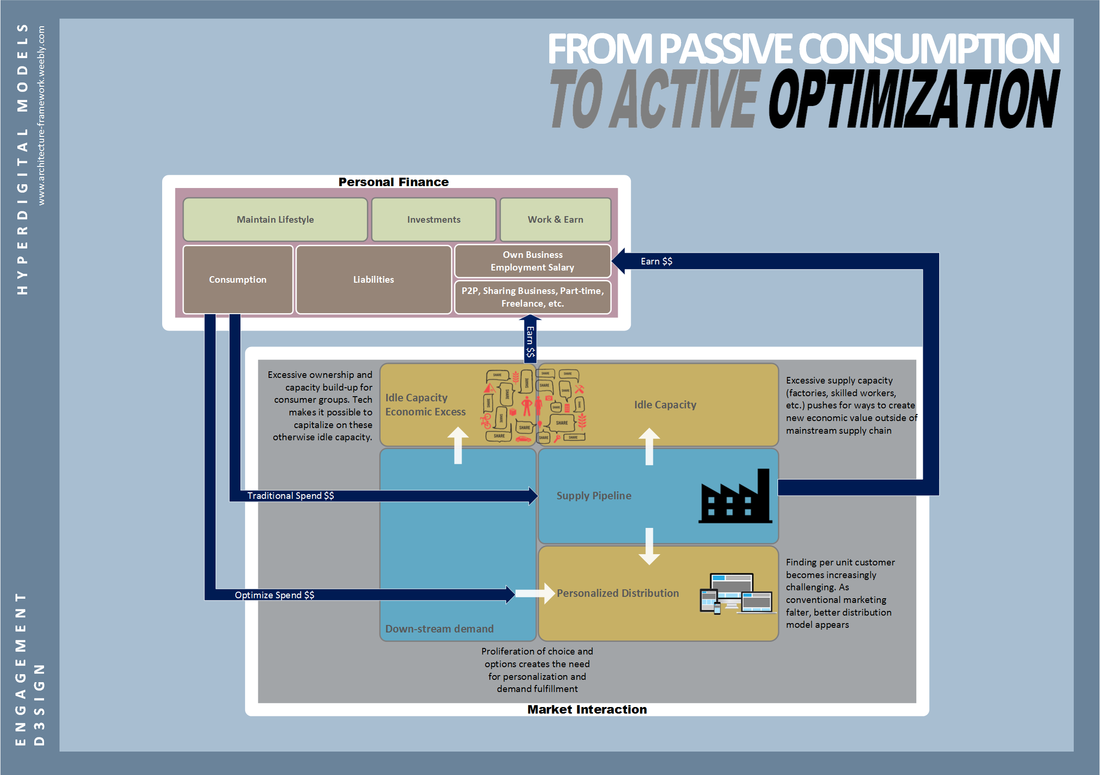

FROM CONSUMER LENDING TO CONSUMER VALUE REALIZATIONAs we slowly move away from the pain of handling physical cash, transaction will eventually be a matter of digits and numbers. When that happens, the net positive or net negative effect of performing that transaction becomes more important than the transaction itself. This presents a profound shift int the mindset of and created a new generation of 'Prosumers'. We have since moved away from passive consumption to one that is continuously optimized and also active in a lot of ways. For instance, sites and services such as ride-sharing, Airbnb, Kickstarter, etc. is also turning professional consumers into producers. Idle hands, idle capacity and idling creative bunches now have the means to generate incomes. The mainstream economic pipe have since spawned the following two hyper-growth engines:

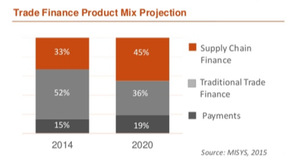

Finding a way to lend to this new ‘prosumer’ group becomes challenging. In such scenario, it is not just cash influx they seek, but the net value exchange they get out of trading or transacting. The challenge for bankers grows as mainstream economy loses share of dollar to this new offshoot market. This is where the e-commerce marketplace players will increasingly find itself in the right spot…….  FROM COMMERCIAL LENDING TO BUSINESS OUTCOME REALIZATIONAs to commercial lending business, today’s downstream SCF (supply chain financing) innovators mostly takes advantage of the scale and ability of e-commerce platform to move goods from supplier to end-customer to generate healthy share of account receivables, a feat that traditional financier are unable to accomplish as they have always separated the 3 components: 1. Logistics of Goods – Buyer responsibility 2. Logistics of Information – Physical document trace needed by bankers 3. Logistics of Money – Key focus of banker On top of that, they are also able to lower inventories as they can rely on more accurate demand data supplied by e-commerce. With SCF projected to continue grow over that of traditional trade finance, it is important that bankers as a source of financing take heed:

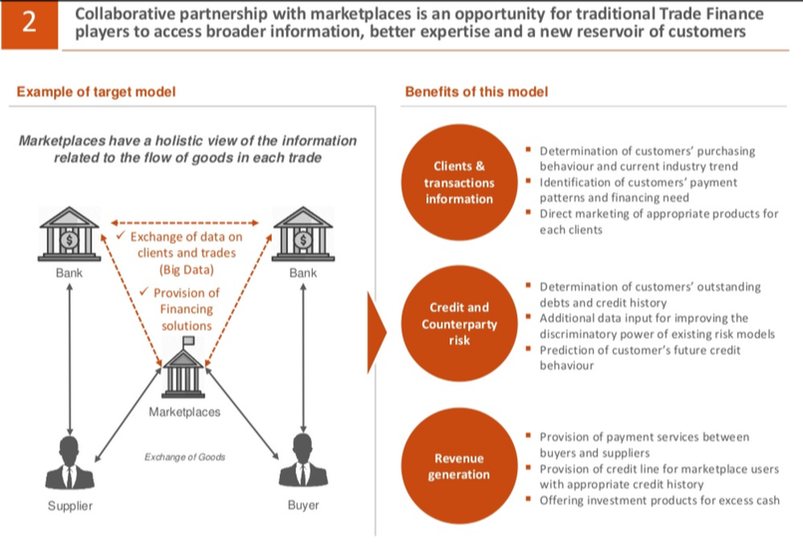

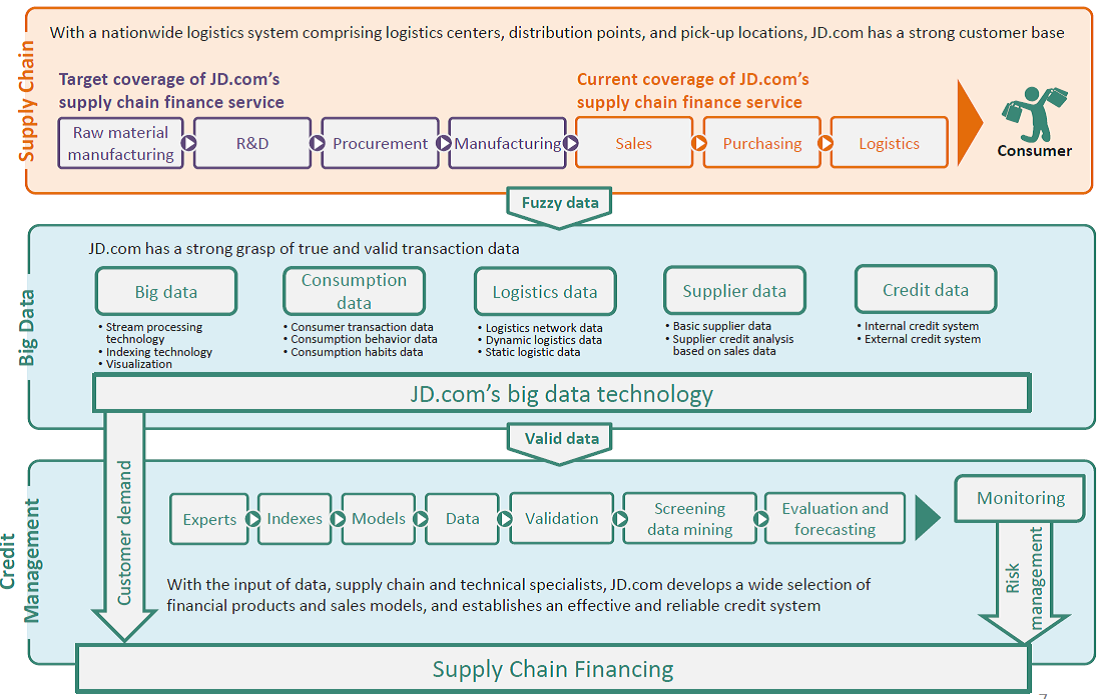

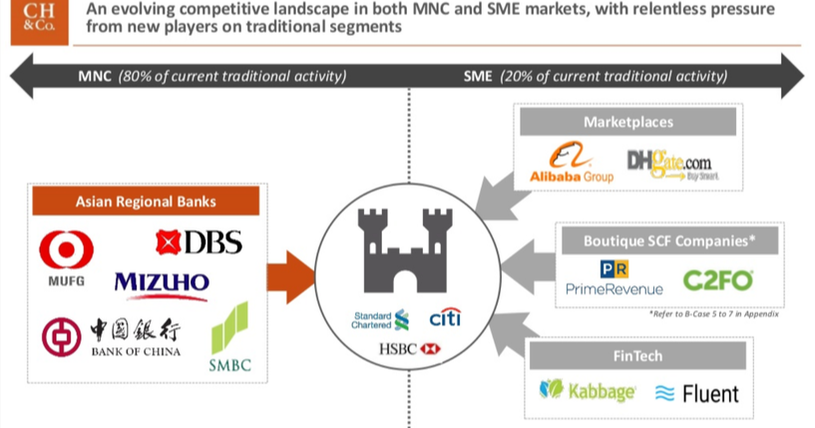

Collaborative SCF (Source: Source: https://www.slideshare.net/CH_APAC_Marketing/trade-finance-in-asia-embracing-the-future) As a result of these platform and through internet ecosystem, innovative disruption is now finding itself swimming upstream. For example, Zhong An insurance helped SME free up working capital by providing return insurance where previously a hefty deposit is required for these merchants to ship on Alibaba platforms. Bankers limited response have been to reduce operating cost, reduce capital cost & credit risk exposures by fostering partnership with marketplace players, e.g. with competing players like Alibaba. In this position, banks will effectively be the payment pipes to release funding and bridging from a KYC, regulatory and currency standpoint.  While much of the disruption is happening for marketplace driven demand chain, there are still sizeable supply-driven and upstream financing requirement. These are more industrial level and larger scale financing needs that is still being fulfilled by bankers. It is in this space where the scope for cost, risk and capital requirement reduction is highest by utilizing technology. Bankers can take a leaf from the strategy chapters of e-commerce players in building the necessary infrastructure that will lay the foundation for more accurate risk management and efficient payment services to their client. Sample operating model can be obtained below (Amazon & JD) “Amazon Lending offers short-term business loans ranging from $1,000 to $750,000 for up to 12 months to micro, small and medium businesses selling on Amazon to help them grow their business…… Traditional lenders shied away from small merchants after the 2008 financial crisis, which created an opening for other sources of financing, including marketplace lenders and other FinTech companies. Amazon has the advantage of being less-tightly regulated than banks and having near real-time data on sellers' businesses and access to their customer reviews. Having this wealth of data minimizes credit risk and is quite important in deciding whether to make a loan.” Source: https://www.cnbc.com/2017/06/16/amazon-plans-to-crush-small-business-lending.html "Supply Chain Finance (Jing Bao Bei): In short, JD's direct sales suppliers sell products to JD, JD then includes these products on its balance sheet under inventory, and expensed on its liabilities under accounts payable, around 40 days payable. After an estimate of 40 days, JD will pay back its suppliers after selling the products. Today, JD doesn't wait 40 days, and will pay suppliers on the day it receives their products. In return. JD will receive 40 days' worth of interests. For suppliers, faster payment means more cash to expand. For JD, it will receive extra income from interests. In terms of accounting, accounts payables will be offset by loans outstanding, with accounts receivable days down by around 5 days. JD disclosed in its 2014 annual a supplier loan balance of 1.5 billion yuan, 15 times its 2013 loan balance of 100 million yuan.”  JD's Supply Chain Finance Service (Source: Fung BI: https://www.fbicgroup.com/)

Other than keeping our money safe and earning diminishing interest returns, the ability to perform transaction and make payments is one of the key reason we choose to deposit money into a particular bank. Banks earn fees from various mechanisms such as overdraft interest, overdue interest, and card interchange fees, payment fees, late charges, etc. These fee-earning schemes gets baked into the likes of payment services, personal loans, micro-credit loans, hire purchase services, instalment services, etc. allowing banks to build a steady base of both interest and fee paying customer. Regulator and technology are now dismantling the tight integration between payment, servicing and deposit accounts. Customers are now open to enjoy the best of these individual services outside of a single bank / service provider. Disintegration of these service bundles is beginning to make banks less attractive and puts pressure on margins when they have to compete on pure play basis, often times using cross-service subsidies or direct discounts.

Today, hyper-scale e-commerce companies such as Amazon and Alibaba have a major share of the retail transaction market. Of late, through its Prime offering, Amazon have successfully turned consumption into repeat subscription funnel. Such moves (and many others to come) may mean one day these players can easily offer competing FI-related services such as small deposits, lending and payment services. Their effective engagement model focusing largely on value extraction and value realization platforms meant they are capable of owning and growing customers day-to-day consumption needs. The ambition and appetite of these technology savvy companies seems insatiable and unstoppable (source: https://thefinanser.com/2014/03/data-wars-why-google-apple-facebook-and-amazon-will-eat-the-bankers-lunch.html). Consider the strategic decisions by these players have already made as far back as 9 years ago:

Some of these services have the unintended effect of turning banks into a ‘dumb pipe’ where customer engagement is further from the moment of truth. Without the engagement, useful data becomes unavailable and may cost banks money to possess in the future. Others are forced and belated reaction by banks to reorganize their services around meaningful customer needs. Yet, the worst kind of actions are the ones that gives valuable data away for short term and temporal returns. There is a sense that a lot of the efforts offered too little too late to reverse the longer term declining trends for bankers. What is missing then? I personally think bankers are largely still grappling with the right operating model in the emerging digital future. A lot of these experimentations are wild shots and often times, desperate media shout outs. They lack of strategic business alignment; poorly designed for learning and experimentation; ill-focused on monetization and not positioned for sustained digital advantage build-up. To understand where bankers are lagging it is worth taking a look inside the actual disruption, i.e. the pace, scale, capabilities and depth of relationship non-banking players are fostering with their customers. E.g. how hyper-digital players continue to bridge the gap and build capabilities for their growing customer base. To ensure sizeable economic benefits are passed on to their customers, they will drive various value-driven customer engagement initiatives at very large scale. This creates attractive value-proposition to customer and in turn attracts capital for continued expansion. Such customer related value initiatives includes:

As you read through the list above, you find little that a bank can offer. Bankers may be caught in a difficult position as they are not e-commerce players and are not allowed to take excessive risk with their clientele’s deposits. Which is probably why China and Singapore government might consider (or is already) allowing bankers there to increase participation in certain non-banking type of risk taking. Other bankers are experimenting with “Banking Inside” approach similar to what Intel has done with its widely successful “Intel Inside” campaign. The approach of building Banking-as-a-Service business model is something fairly new and will take time to prove viable. Banks need to build a sizeable ecosystem and an extensive knowledge of their partner/customer in order to become a viable core platform (e.g. see BBVA’s approach to API). It is however, limited response from the banking community. They are largely taking a fringe position from core innovation happening in the actual market place. China is already providing the world a glimpse of what is going to happen to traditional banking in the face of relentless innovation pursuit by tech players there. For example, news headline such as: “China’s Banks lost $22B to Alibaba and Tencent in 2015, But that’s not their Biggest Problem”. Source: https://www.forbes.com/sites/zennonkapron/2016/03/06/china-banks-lost-22b-to-alibaba-and-tencent-in-2015-but-thats-not-their-biggest-problem/#4f4e69ae6094 Things will get worst not just for bankers but for other retailers and brand owners once voice or image based search comes into play as it offers unprecedented opportunity for these tech players to both harvest data and engage customers. As these AI’s build trust and advancements, customer will grow more comfortable and dependent on built-in recommendations to help make day-to-day consumption decisions. Such gatekeeper devices, being imageless and textless, will essentially mask away complexity associated with the traditional brand medias and turn consumption into ‘noise-free’ and ‘frictionless’ experience (source: L2's Scott Galloway’s presentation here: https://www.youtube.com/watch?v=GWBjUsmO-Lw). In this scenario, most brands (banks included) will become mere ‘dumb pipes’ of goods and services, all to the advantage of marketplace platform innovators. The relief is, banks are not alone. |

AuthorDavis Chai is an Architect in the FSI industry for the past 10 years. His career involvement in the industry informed his work and allowed him to contribute to this blog. Archives

September 2017

|

RSS Feed

RSS Feed