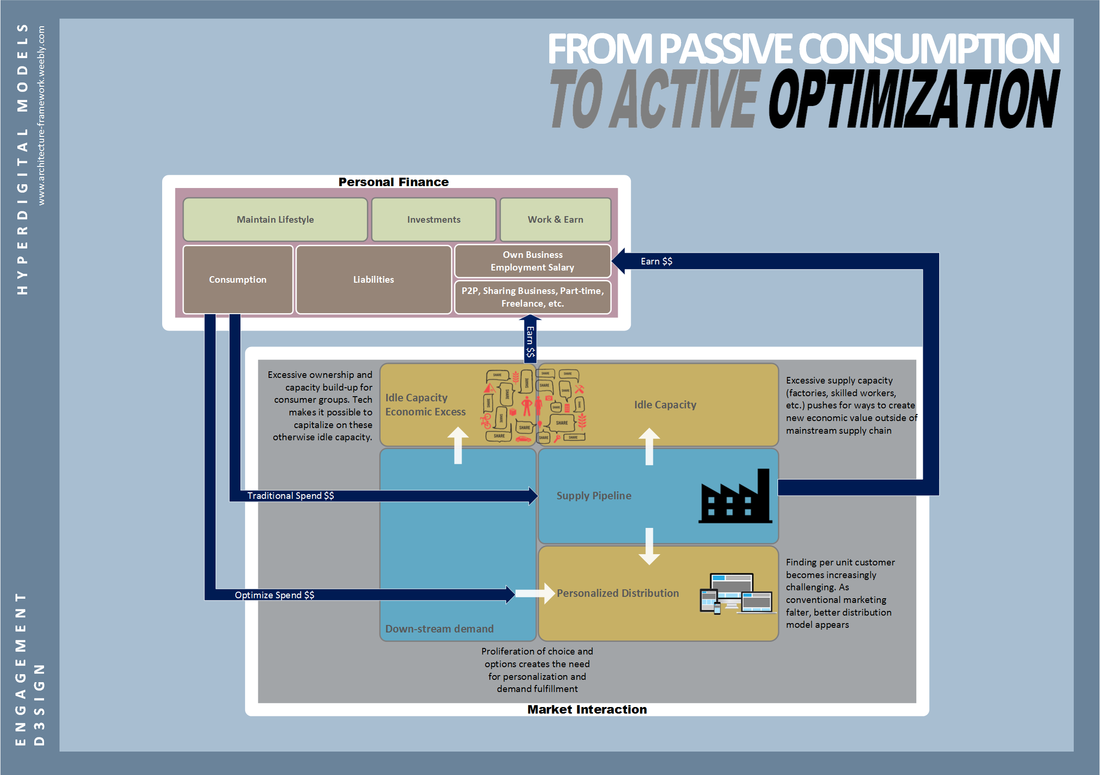

FROM CONSUMER LENDING TO CONSUMER VALUE REALIZATIONAs we slowly move away from the pain of handling physical cash, transaction will eventually be a matter of digits and numbers. When that happens, the net positive or net negative effect of performing that transaction becomes more important than the transaction itself. This presents a profound shift int the mindset of and created a new generation of 'Prosumers'. We have since moved away from passive consumption to one that is continuously optimized and also active in a lot of ways. For instance, sites and services such as ride-sharing, Airbnb, Kickstarter, etc. is also turning professional consumers into producers. Idle hands, idle capacity and idling creative bunches now have the means to generate incomes. The mainstream economic pipe have since spawned the following two hyper-growth engines:

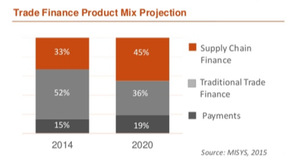

Finding a way to lend to this new ‘prosumer’ group becomes challenging. In such scenario, it is not just cash influx they seek, but the net value exchange they get out of trading or transacting. The challenge for bankers grows as mainstream economy loses share of dollar to this new offshoot market. This is where the e-commerce marketplace players will increasingly find itself in the right spot…….  FROM COMMERCIAL LENDING TO BUSINESS OUTCOME REALIZATIONAs to commercial lending business, today’s downstream SCF (supply chain financing) innovators mostly takes advantage of the scale and ability of e-commerce platform to move goods from supplier to end-customer to generate healthy share of account receivables, a feat that traditional financier are unable to accomplish as they have always separated the 3 components: 1. Logistics of Goods – Buyer responsibility 2. Logistics of Information – Physical document trace needed by bankers 3. Logistics of Money – Key focus of banker On top of that, they are also able to lower inventories as they can rely on more accurate demand data supplied by e-commerce. With SCF projected to continue grow over that of traditional trade finance, it is important that bankers as a source of financing take heed:

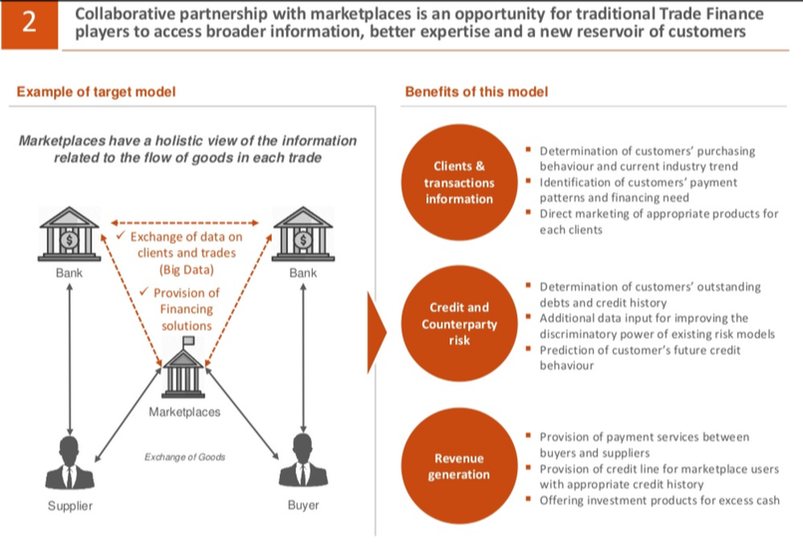

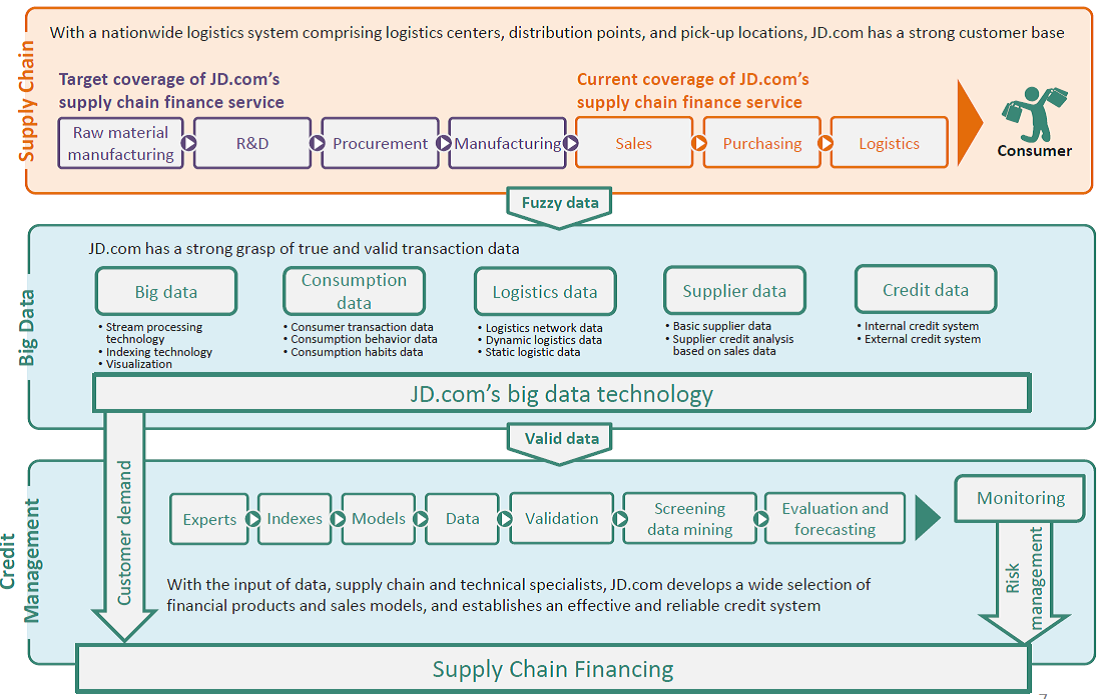

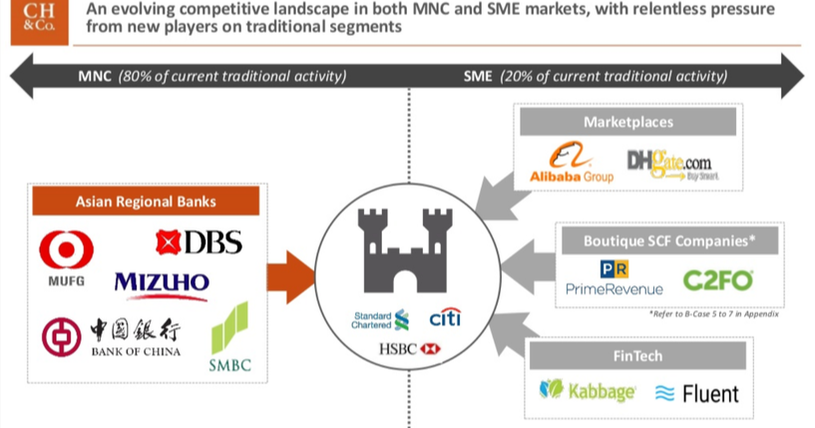

Collaborative SCF (Source: Source: https://www.slideshare.net/CH_APAC_Marketing/trade-finance-in-asia-embracing-the-future) As a result of these platform and through internet ecosystem, innovative disruption is now finding itself swimming upstream. For example, Zhong An insurance helped SME free up working capital by providing return insurance where previously a hefty deposit is required for these merchants to ship on Alibaba platforms. Bankers limited response have been to reduce operating cost, reduce capital cost & credit risk exposures by fostering partnership with marketplace players, e.g. with competing players like Alibaba. In this position, banks will effectively be the payment pipes to release funding and bridging from a KYC, regulatory and currency standpoint.  While much of the disruption is happening for marketplace driven demand chain, there are still sizeable supply-driven and upstream financing requirement. These are more industrial level and larger scale financing needs that is still being fulfilled by bankers. It is in this space where the scope for cost, risk and capital requirement reduction is highest by utilizing technology. Bankers can take a leaf from the strategy chapters of e-commerce players in building the necessary infrastructure that will lay the foundation for more accurate risk management and efficient payment services to their client. Sample operating model can be obtained below (Amazon & JD) “Amazon Lending offers short-term business loans ranging from $1,000 to $750,000 for up to 12 months to micro, small and medium businesses selling on Amazon to help them grow their business…… Traditional lenders shied away from small merchants after the 2008 financial crisis, which created an opening for other sources of financing, including marketplace lenders and other FinTech companies. Amazon has the advantage of being less-tightly regulated than banks and having near real-time data on sellers' businesses and access to their customer reviews. Having this wealth of data minimizes credit risk and is quite important in deciding whether to make a loan.” Source: https://www.cnbc.com/2017/06/16/amazon-plans-to-crush-small-business-lending.html "Supply Chain Finance (Jing Bao Bei): In short, JD's direct sales suppliers sell products to JD, JD then includes these products on its balance sheet under inventory, and expensed on its liabilities under accounts payable, around 40 days payable. After an estimate of 40 days, JD will pay back its suppliers after selling the products. Today, JD doesn't wait 40 days, and will pay suppliers on the day it receives their products. In return. JD will receive 40 days' worth of interests. For suppliers, faster payment means more cash to expand. For JD, it will receive extra income from interests. In terms of accounting, accounts payables will be offset by loans outstanding, with accounts receivable days down by around 5 days. JD disclosed in its 2014 annual a supplier loan balance of 1.5 billion yuan, 15 times its 2013 loan balance of 100 million yuan.”  JD's Supply Chain Finance Service (Source: Fung BI: https://www.fbicgroup.com/)

0 Comments

Leave a Reply. |

AuthorDavis Chai is an Architect in the FSI industry for the past 10 years. His career involvement in the industry informed his work and allowed him to contribute to this blog. Archives

September 2017

|

RSS Feed

RSS Feed