|

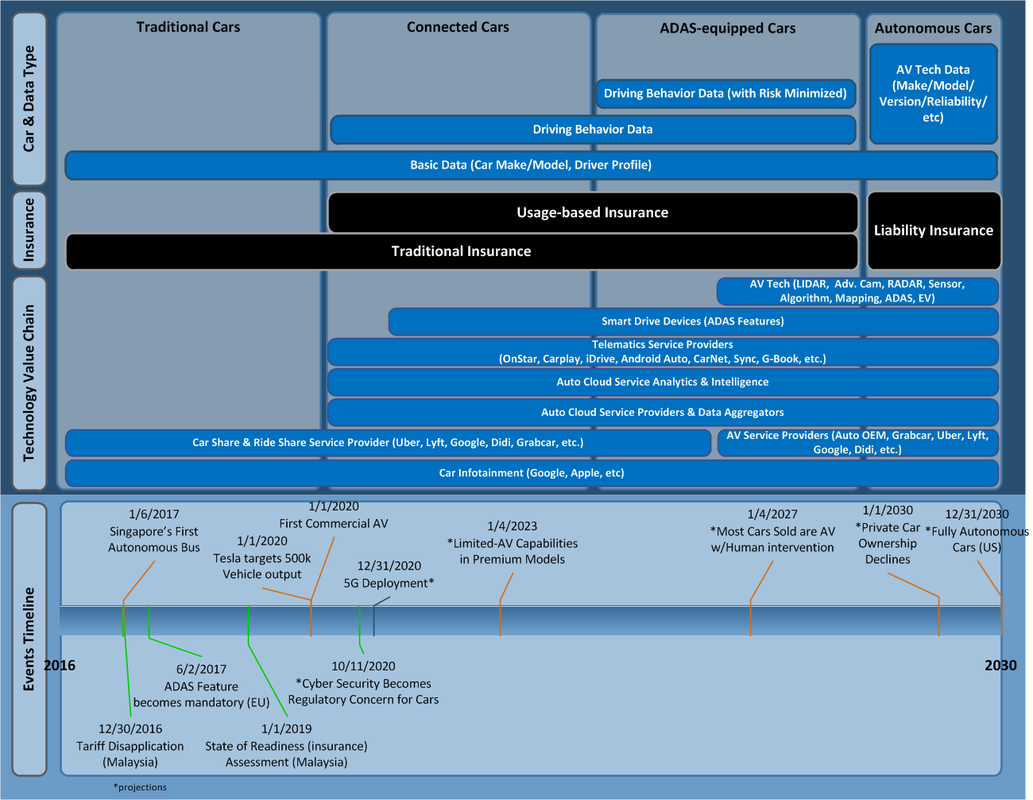

"While standalone telematics insurance solutions have been in various markets for a while, data from built-in car sensors and systems will be part of a new generation of real-time motor insurance in future. Today, emergency rescue services can be alerted automatically about location and severity in case of an accident. In future, health insurance companies would be notified, first estimations about damaged car parts can be transmitted to insurance companies and repair shops in real-time while new black box generations will allow loss adjusters to better understand the circumstances of the accident" - Mr. Fang, as the Chief Underwriting Officer, PICC P&C (source: munichre.com)  Players in the Auto industry (i.e. OEMs and insurance providers) are bracing themselves not only for the impact of regulatory changes but also the larger shift in the industry caused mainly by technological advancement. The ASEAN region will likewise be disrupted as early as 2020 and the local market players must respond or become irrelevant as the last wave of traditional car refresh projected to take place post-2030 in more advanced countries. As the value shifts, previously unheard of players will become prominent in the auto industry such as cloud service providers in the form of SaaS and smart device OEMs.

For the insurance sector, one of the major push for deregulation (in Malaysia) has been the unsustainable high third-party claim rate and theft rate. Regulators have opted for a phased approach having in mind the price hike that will be triggered on these auto-insurance policies. There are substantial barriers (both structural and social factors) to overcome , For example, the perceived higher average car age and the lack of capabilities of insurance players to offer risk and behavior adjusted insurance policies. The higher retained value of aging car (up to 40%, source: freemalaysiatoday.com) presents a socio-economical challenge to regulators who wants to make meaningful and socially inclusive regulatory change. Steps needs to be put in place to change this as these high-risk vehicles will become a drag to the entire industry. Even though the impact of Self-driving car is not going to be felt in another 10 year or so the opportunity to change and adapt is right here and right now. Regulator plays pivotal role in driving this change. Players who are responding to rapid market shift can best do so when working closely with the industry association and regulators - which best explains why the current MY round of tariff deregulation is mostly consultative and in step-phases. NOTE: This is a quick take of the auto and auto insurance market, with more focus on the Malaysia side of the market as well as projected technology evolution. The timeline data and dates are mostly projections from multiple unverified sources.

0 Comments

|

AuthorDavis Chai is an Architect in the FSI industry for the past 10 years. His career involvement in the industry informed his work and allowed him to contribute to this blog. Archives

September 2017

|

RSS Feed

RSS Feed