Banking Evolution

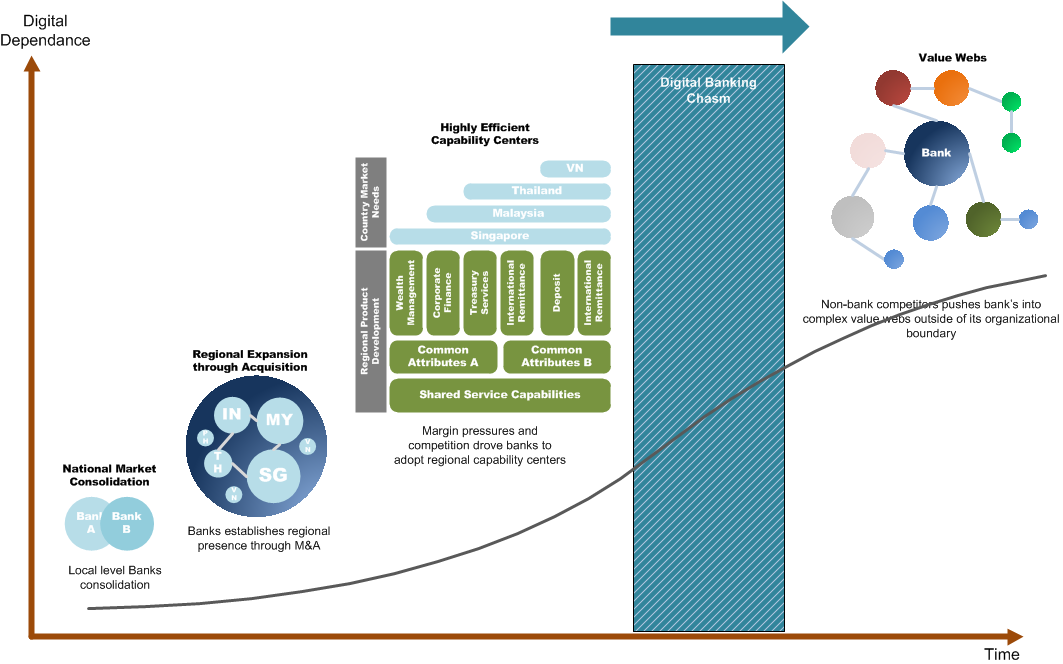

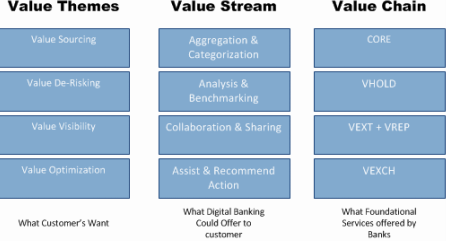

Most banks started off as small local community banks. By using branch as they expansionary engine, banks were able to extend their presence beyond its local community. Whether through acquisition or by organic growth, some of these banks grew and evolved into national level banks. The larger scope required investment in national level business capabilities that utilizes technologies and standardized processes. As trade expanded and governments gradually deregulated banking, further acquisition and mergers at the regional level made it feasible for larger regional banks to exist. To be effective, the newly formed regional banks have to develop different operating models in order to fulfill different legislative and market maturity needs. This lead to the creation of regional shared service centers (SSC) and regional center of excellence (RCOE). Such larger scale and scope enables banking to operate at a higher efficiency level while at the same time compete effectively with regional peers and global operators. With the onset and growth of internet services, a new form of banking that extends the reach and banking efficiency is starting to take form. This time, it is highly digital in nature. Digital Banking Chasm The term first coined for Geoffrey A. Moore’s book: “Crossing the Chasm: Marketing and Selling High-Tech Products to Mainstream Customers” that points to the most difficult step in making the transition between visionaries (early adopters) and pragmatists (early majority). The Chasm is the foundation for which value web benefits can be realized; it enables transformation from traditional banking to highly personalized banking service (Value Web).This required banks to look at digital banking experience in its entirety - from a digital banking ecosystem perspective. Digital banking ecosystem is where the entire service model will be redefined around that of the Value Chain and Value Stream (http://architecture-framework.weebly.com/banking/banking-value-chain). The 2 value functions takes full advantage of MAGICS (Mobile, Analytic, Gamification, IoT, Cloud & Social) in order to satisfy customer’s value needs. For the service ecosystem to be effective, banks have to create a digital experience which is highly adaptive, responsive and continuous in nature. We identifies a set of common value needs to will help banking service providers to map into customer value needs. Customer Value Needs Customer value needs is identifiable by a set of common themes - hence the term Value Themes. These Value Themes are:

Banking ecosystem is more like a branded concept than a product strategy. It follows the way that customer uses banking services. When a person wakes up in the morning, his digital wallet reminds him of how much he should be spending where (actionable insights) - VVSI. While driving on his way to work, he runs into a petrol to refill his gas tank and pays using mobile phone by NFC payment. He instantly receives an update on his spending pedometer via a mobile app - VVSI. He sees that he is spending within his limits - VDRISK. During his workday, he gets prompted of due bills via his mobile app and instantly verify and paid within 2 clicks (API banking). He notices that his balance is looking strong and decides to lend out to make quick bucks - VOPTI. He utilizes the bank recommended crowd-lending platform to lend out about USD1000 to earn USD50 return after 3 months (for 5% interest). He scores a match and approves the lending on his phone - VSORC. By the end of his work day, he receives a cheque for his travel claim. He uses his banks mobile app and banks in the cheque by taking an image of the cheque and sending it to the bank. His PFM pedometer shows his 1-day floating balance - VVSI. At home, his son called and requests for additional fund to cover for expenses. He instantly sends the fund through his son’s debit account (free of charge). By the end of the day, he projects his son’s spending using a linked-account PFM and sees that he is overspending his meal allowances - VVSI. He calls his son and had a quick and discover that his son is actually dating a new girlfriend. He explains to him that the additional spending will eat into following month allowances if he can't control it. By the end of the week, he receives an emergency call that one of his parents needs to go for a surgery and needed funding. After exhausting his options, he decides to seek funding through his crowd-lending platform but discovered that it is above the lending limits - VSORC. Bank discovered it and offers him alternate funding through bank loans - a low interest non-collateral loan.

0 Comments

As a follow-up to our earlier posting on Customer Driven CRM Mobile App, we propose the architecture elements that enables such CRM app to function. These elements should drive the development of people structure and processes with an effective IT capability as the foundation.

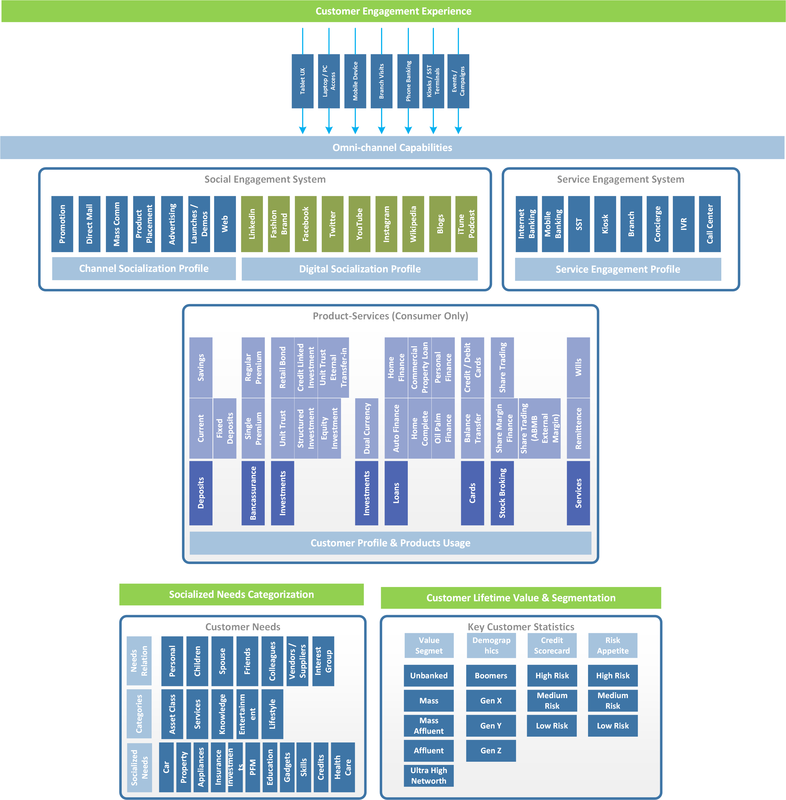

Customer Touchpoints Most organization differentiate between sales engagement and client support engagement. Others have additional functionality around marketing engagement. With mobile and digital technologies, all these functional differences are proving to become a challenge as they continue to function in silo. This is proving costly for banks as all these function are supposed to create a single ‘customer engagement’ capability when combined. For analytic to be effective, all these client facing organization needs to channel their engagement information into a single customer oriented profile. In a nutshell, these profiles are:

Social (Channel & Digital) Engagement Profile Traditional marketing approach advocates non-interactive features such as direct mail, mass media communication, telemarketing, etc. offers little relevance to the individual customer. With such things as spam filters and advertising clutters, customers are increasingly finding the approach annoying (transition phase). The inclusion of social channels as part of banking social engagement strategy is required. Banks have even started to bundle the marketing and socialization messages using banking and e-statements to reduce attrition. By creating a presence and by expanding data analytic into the social space, banks now have an added dimension from which they can evaluate customer value potential and improve share-of-wallet with customer. This could be accomplished through embedding various social channel API’s into purpose built consumer mobile app. At the same time, traditional marketing approach is still used for engaging general mass market customer. Service Engagement Profile It is in the direct customer engagement services where banking relationship is formalized. Customers engagement experience should be assessed and the result of the assessment forms the engagement profile. These are accomplished through a combination of various machine systems (banking portals and self-service terminals) and client engagement workforce (i.e. branch system). The interaction and quality of the interaction has traditionally been measured on a silo perspective. This, in the face, of rising digital importance, is inadequate. The direct channel engagement experience needs to be benchmarked and correlated with data gathered from the other profiles. Client engagement data can provide useful insights in many ways, for example:

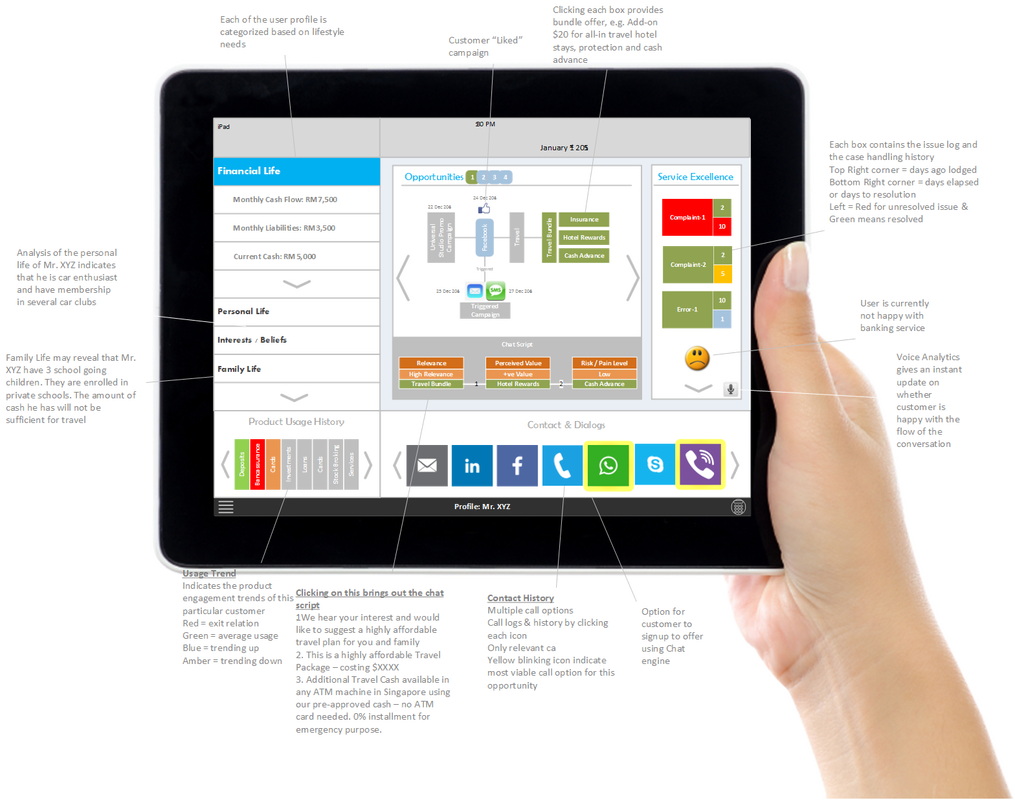

Combining Social & Service Engagement Profile When information from both social-digital and channel fabric is combined and used to compute a particular client’s profile, it offers a greater perspective to a client’s lifestyle and service consumption needs. Using techniques such as targeted promotions, socially driven campaigns, purpose built application, etc. a bank is able to construct the needs of the customer. For instance, using Facebook for a marketing campaign, a customer's preference can be mapped when he or she clicks the ‘like’ button on the social message board. This gives the bank a snapshot of the person’s resource motivations. Product Usage Profile Through the use of banking product and services, an individual customer makes available to the bank critical personal information. Although, protected by privacy laws, the underlying bank have the liberty to make use of the data for internal purposes. For this profile, bank needs to capture key information such as the demographics, customer asset and liabilities, collateral, card ownership, car ownership, mortgages, purchasing habits, financial needs, their relationship with other customer, etc. The output of product usage profile needs to translate to customer lifetime value. This quantitative view of the customer enables the bank to evaluate its potential value and its risk to the bank. Such mapping can then be used to target certain customer for further product-mapping and segmentation. Customer Relationship Officers armed with Tablet displaying real-time CRM information can go a long way in improving customer acquisition and customer retention. One such as the following:  Imagine for a while now that the customer engagement officers, whether they are located in branches, in kiosks location or in contact centers, gets the same CRM data and interface. All of them get instant up-to-date access to the same customer information on the go. This 360 degree view of the customer is real-time across all service channels (omni-channel).

The interface is designed to drive customer service behavior using analytics. The system serves as both an output and input device. Customer profile and engagement statistics will be updated instantly after each and every engagement. This is done by manual entry of the officer as well as by data captured through out the conversation. Individual customer statistics are can then be aggregated to form a larger segment profile and banking service trend. LIFESTYLE PANE This pane provides vital information regarding each lifestyle areas of the customer. For instance, the financial core of the customer is shown herein to indicate his or her debt level, liabilities, cashflow and asset information. Dragging the financial life pane to the middle will display more customer financial information. This is useful for instance if a customer intends to find out if early repayment of a hire-purchase loan is possible. Due to the analytical nature of this application, an additional button prompts the customer service officer to find out how customer can better use the early redemption funds. The click of that button sends the financial scoring system to scour for other relevant information and return with several funding use cases - such as saving in high-interest earning account for child education or invest in medical insurance for aging parents that appears to medical care. Such highly interactive way of socializing customer information ensures that customer servicing agents are focused on one thing - customer service. Other non-financial information can also be displayed such as family-life information. Through interaction and social analytic, the customer family life tab can be populated with relevant information such as direct and distant family members, travel lifestyle, child education and school information, hometown location, hometown visits, etc. USAGE TREND INDICATORS Shows the level of customer engagement in any of the key product services offered by this bank. The statistics captures number of customer access to each banking function, visit to the site or branch for a particular service (e.g. ATM withdrawals, cheque transfers, payments), the calls made to service center to lodge a issue or enquiry, etc. This information will only be useful if the engagement can be further broken down to specific product or service areas. Service engagement and product engagement are intertwined, when combined it may produce positive or negative customer perception. Usage trend and service excellence is combined to form a trend line. Trend line can be visualized in such a way that it coincides with an incident. SERVICE EXCELLENCE PANE The service usage stats leads to another critical insight. - service quality. By taking into account key measurements such as the number of call/interaction logged, the number of issues resolved, the turnaround time in resolving issues, the customer service agents can now relate to the individual customer’s usage experience. More importantly, customers final score of satisfaction is is shown in this pane. Such data can be calculated on an averaging basis. The analytical models need to be tuned over time to take into account customer perception after a promotional and good-feel campaign. To make it relevant, the scoring system can analyze the voice of customer and baseline their receptiveness to new offers. A simple smiley icon can potentially be used to indicate the satisfaction score. Such feedback mechanism allows customer interaction officer to proactively take measures to make the engagement more positive - even if the engagement does not lead to new sales. CONTACT & DIALOG BOX The contact and dialog box offers customer service agent a peek into the history of customer engagement and using which medium of contact. Even here, the dashboard can be highly interact in that whenever a customer is seen online or is seen to have repeated responded through a particular channel, that channel becomes the preferred contact option. The app goes further in notifying the agent the best way to contact a customer by blinking and highlighting the contact option. To make reduce clutter, the app will actively hide contact option that is deemed as ineffective or irrelevant in getting customer response. This is useful in an environment where communication options are vast. OPPORTUNITY DIALOG BOX Perhaps the most important component of the CRM dashboard is the opportunity window. Any engagement with customer should lead to one of 2 aspects of the relationship: 1. Improved sales (up-sell or new sales) 2. Improved customer service perception that will: a. create a more conducive environment to improve sales in subsequent engagement. b. improve customer retention. In order to be able consistently increase customer wallet shares, the analytical engine need to churn out sales opportunities in alignment to actual customer perceived needs. The underlying analytics rely on social engagement data inputs. The earlier discussed social and digital engagement systems provides the necessary data inputs necessary to formulate lifestyle needs of the individual customer. Under the opportunity window is the sales and approach script. This script is a workflow engine that combines the most likely element of acceptance into sequential steps. This is based on the learning framework and internalization concept briefly mentioned in my first posting on Banking Value Chain . My next blog update will show what architecture elements and data profiles are required to build this type of app. Stay tuned! This PDF article discusses about the recent technology and Fintech's impact in the consumer banking industry. It proposes a structure for which to analyse the relative positions of each player in the banking technology space. |

AuthorDavis Chai is an Architect in the FSI industry for the past 10 years. His career involvement in the industry informed his work and allowed him to contribute to this blog. Archives

September 2017

|

RSS Feed

RSS Feed