Banking Evolution

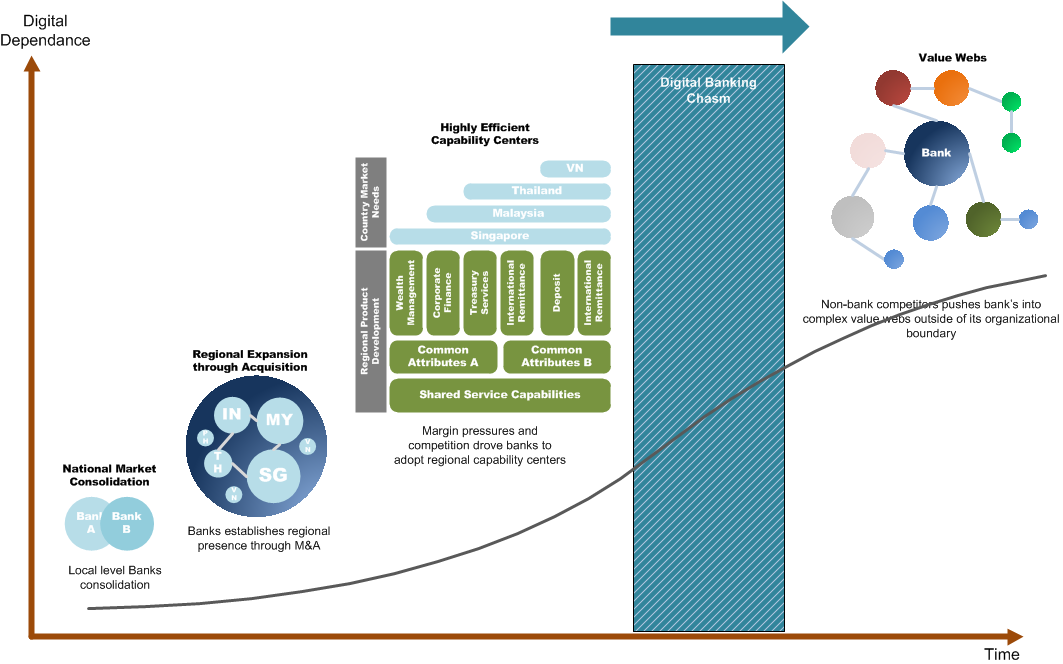

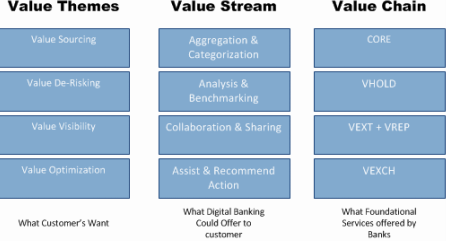

Most banks started off as small local community banks. By using branch as they expansionary engine, banks were able to extend their presence beyond its local community. Whether through acquisition or by organic growth, some of these banks grew and evolved into national level banks. The larger scope required investment in national level business capabilities that utilizes technologies and standardized processes. As trade expanded and governments gradually deregulated banking, further acquisition and mergers at the regional level made it feasible for larger regional banks to exist. To be effective, the newly formed regional banks have to develop different operating models in order to fulfill different legislative and market maturity needs. This lead to the creation of regional shared service centers (SSC) and regional center of excellence (RCOE). Such larger scale and scope enables banking to operate at a higher efficiency level while at the same time compete effectively with regional peers and global operators. With the onset and growth of internet services, a new form of banking that extends the reach and banking efficiency is starting to take form. This time, it is highly digital in nature. Digital Banking Chasm The term first coined for Geoffrey A. Moore’s book: “Crossing the Chasm: Marketing and Selling High-Tech Products to Mainstream Customers” that points to the most difficult step in making the transition between visionaries (early adopters) and pragmatists (early majority). The Chasm is the foundation for which value web benefits can be realized; it enables transformation from traditional banking to highly personalized banking service (Value Web).This required banks to look at digital banking experience in its entirety - from a digital banking ecosystem perspective. Digital banking ecosystem is where the entire service model will be redefined around that of the Value Chain and Value Stream (http://architecture-framework.weebly.com/banking/banking-value-chain). The 2 value functions takes full advantage of MAGICS (Mobile, Analytic, Gamification, IoT, Cloud & Social) in order to satisfy customer’s value needs. For the service ecosystem to be effective, banks have to create a digital experience which is highly adaptive, responsive and continuous in nature. We identifies a set of common value needs to will help banking service providers to map into customer value needs. Customer Value Needs Customer value needs is identifiable by a set of common themes - hence the term Value Themes. These Value Themes are:

Banking ecosystem is more like a branded concept than a product strategy. It follows the way that customer uses banking services. When a person wakes up in the morning, his digital wallet reminds him of how much he should be spending where (actionable insights) - VVSI. While driving on his way to work, he runs into a petrol to refill his gas tank and pays using mobile phone by NFC payment. He instantly receives an update on his spending pedometer via a mobile app - VVSI. He sees that he is spending within his limits - VDRISK. During his workday, he gets prompted of due bills via his mobile app and instantly verify and paid within 2 clicks (API banking). He notices that his balance is looking strong and decides to lend out to make quick bucks - VOPTI. He utilizes the bank recommended crowd-lending platform to lend out about USD1000 to earn USD50 return after 3 months (for 5% interest). He scores a match and approves the lending on his phone - VSORC. By the end of his work day, he receives a cheque for his travel claim. He uses his banks mobile app and banks in the cheque by taking an image of the cheque and sending it to the bank. His PFM pedometer shows his 1-day floating balance - VVSI. At home, his son called and requests for additional fund to cover for expenses. He instantly sends the fund through his son’s debit account (free of charge). By the end of the day, he projects his son’s spending using a linked-account PFM and sees that he is overspending his meal allowances - VVSI. He calls his son and had a quick and discover that his son is actually dating a new girlfriend. He explains to him that the additional spending will eat into following month allowances if he can't control it. By the end of the week, he receives an emergency call that one of his parents needs to go for a surgery and needed funding. After exhausting his options, he decides to seek funding through his crowd-lending platform but discovered that it is above the lending limits - VSORC. Bank discovered it and offers him alternate funding through bank loans - a low interest non-collateral loan.

0 Comments

Leave a Reply. |

AuthorDavis Chai is an Architect in the FSI industry for the past 10 years. His career involvement in the industry informed his work and allowed him to contribute to this blog. Archives

September 2017

|

RSS Feed

RSS Feed