|

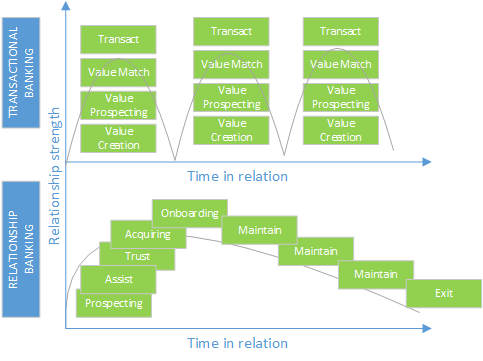

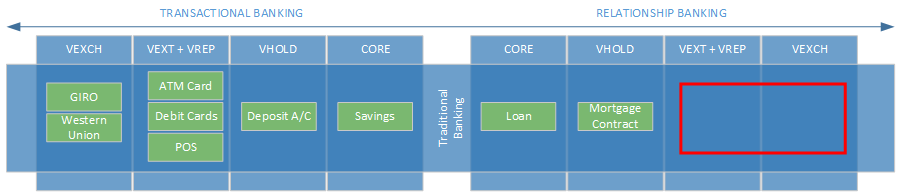

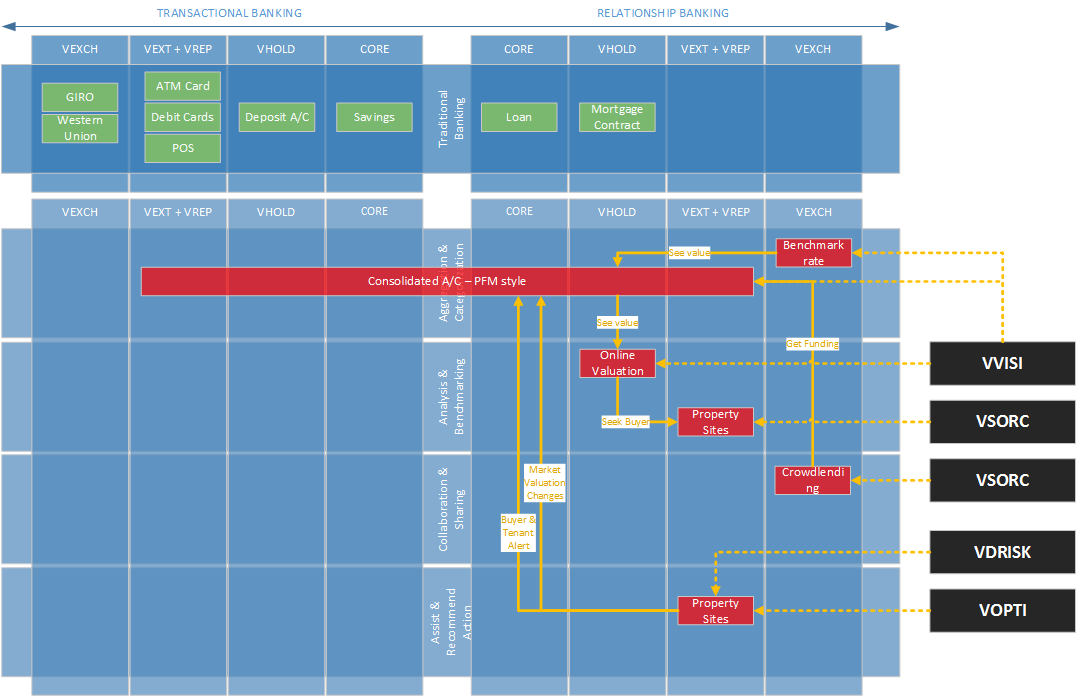

The digital world (when combined with other elements of banking) offers a way to bridge product gaps that have long existed in Banking. Consider the case of Relationship banking product and Transactional banking product. Payment and card based services which is transactional in nature versus priority banking, mortgage, hire purchase and insurance products which is relationship in nature. Customer lifecycle experience in both type of product is asymmetrical in nature. In relationship banking, the cost of sale is usually frontloaded where customer engagement is usually heavy in the initial phase of the relationship. However, the engagement efforts usually tapers down as bank and customer enters a 'maintain' phase. This, compared with transaction banking is completely different - where each and every transaction means that banks must resolve to use every channel at its dispose to create value in order to sustain the Transactional relationship - one transaction at a time. The relationship either improves or degrades by each transaction.  Relationship Banking (RB) can easily borrow the techniques used by Transaction Banking (TB) to improve customer loyalty and prevent profitability 'leakage'. If you compare both TB and RB from a Value Chain perspective, there is no way that RB products such as mortgage, insurance & hire purchase can have an effective Value Extraction Value Representation component as these are not your typical day-to-day transaction items. NOTE: This article references concepts discussed in earlier articles in this blog. To better understand the concept discussed herein, at a minimum, read the blog on Value Themes & Banking Value Chain: /banking.html  With traditional banking, its simple not possible to offer any VEXT and VREP capabilities to RB products. However, by adding digital capabilities into the mix, interesting combination will emerge. We begin by overlaying Value Stream and Value Themes onto RB product and explore ways to create better engagement with clients.  Through partnership and in-house data mining, banks can offer various VEXT, VREP and even VEXCH capabilities to their clients. For instance, banks could offer functionality for clients to check the market valuation for their property (mortgage loan) from time to time or via notifications, thereby enabling VVISI in clients portfolio. The result of the valuation can be used by the client to post "for sale" offer through a 3rd party site/agency. All these could be done digitally by way of mobile application. This allows the customer to constantly engage the market and test the value of their property. Any interest from the market will result in notification to the client through banking or third-party app. For the bank, it is important that data is retained regarding the market that this client is engaged - which could be used for client retention engagement or broader market positioning purposes. The key here is in tightly integrating customer experience in the product/service category to the value ecosystem that a bank offers.

Many more option is available to improve the state of the RB products. The diagram offers several lessons that RB can learn from TB in the digital world.

0 Comments

Leave a Reply. |

AuthorDavis Chai is an Architect in the FSI industry for the past 10 years. His career involvement in the industry informed his work and allowed him to contribute to this blog. Archives

September 2017

|

RSS Feed

RSS Feed